Retail at the Breaking Point-STRATEGIC TRENDS ANALYSIS 2026

Retail has reached a structural breaking point. Seven forces are converging simultaneously, each reinforcing the others, each demanding a response that goes beyond incremental improvement. This analysis — synthesized from Gartner, McKinsey, Accenture, Deloitte, NRF, WEF, IDC, and direct operator intelligence from Walmart, Amazon, JioMart, Costco, and the NRF Top 50 — is designed to be the definitive strategic trends analysis for retail leaders who need to act in 2026.

Key Statistics from the Research Corpus

Master Trend Map: All 44 Trends at a Glance

The 7 Meta-Forces: A Framework for Understanding Structural Change in Retail

Most industry trend reports list observations. This analysis identifies forces — causal mechanisms that are reshaping the structural economics, competitive dynamics, and consumer relationships of retail. A trend describes what is happening. A meta-force explains why it cannot be reversed, why it compounds over time, and why leaders who ignore it face existential consequences.

The Selection Methodology

A force earns a place in this framework if it meets three criteria: (1) It is structural, not cyclical — it does not reverse when macroeconomic conditions change. (2) It has compounding effects — the advantage of early movers grows over time, and the cost of delay increases. (3) It forces a binary choice — retailers cannot remain neutral; every month of inaction is itself a strategic decision.

The 7 Forces at a Glance

How the 7 Forces Interact: The Causal Logic

The convergence of all seven forces simultaneously is what creates the “breaking point” framing. In prior decades, retailers faced one or two structural forces at a time. The 2026 environment is characterized by all seven operating concurrently and reinforcing each other — which is why the urgency is different from any previous transformation cycle.

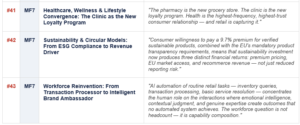

Meta-Force 1: Agentic AI & The New Commerce Operating System

Trend Summary

Trend Deep-Dives

Trend #1 — Google Universal Commerce Protocol: The Standard That Defines AI Commerce

WHY THIS EXISTS

Google launched UCP at NRF 2026 co-developed with Shopify, Walmart, Target, Wayfair, Etsy; endorsed by 20+ partners including Mastercard, Visa, Stripe. Salesforce: AI agents influenced 20% of 2025 holiday season orders. Adobe: GenAI holiday traffic surged 693% YoY. Conversational commerce projected to reach $290B globally by 2027. UCP enables AI to handle the full purchase journey — from discovery through checkout through post-purchase support — without the consumer leaving a chat window.

BUSINESS IMPACT

• Retailers not integrated with UCP risk invisibility to AI agents processing purchases for hundreds of millions of consumers

• Native checkout inside Google Search AI Mode and Gemini is live for eligible US retailers — Microsoft Copilot embedded checkout launched simultaneously

• The protocol is already powering transactions: Lowe’s, Michael’s, Poshmark, and Reebok were live at launch

• Only 17% of consumers currently comfortable letting AI complete a full purchase (ChannelEngine, 4,500 shoppers) — the adoption curve accelerates as AI accuracy improves

STRATEGIC IMPLICATIONS

• Integrate UCP as a strategic infrastructure decision, not a technical project — the data standards it sets will determine AI agent visibility for years

• Treat structured product data, real-time pricing feeds, and inventory APIs as consumer-facing assets that require the same investment as the website

• Develop explicit agentic commerce governance: what is your brand’s rules-of-engagement for AI agents transacting on your behalf?

Trend #2 — Proprietary AI Intelligence: Training on Owned Data Creates Durable Competitive Separation

WHY THIS EXISTS

Walmart consolidated AI tools into four domain-specific super-agents — customer, associate, supplier, developer — powered by Wallaby, retail-specific LLMs trained on decades of Walmart proprietary data (Reuters July 2025). Amazon’s Rufus AI merchant is trained on product data, customer reviews, and purchase history across 600M+ SKUs. Gartner: 40% of enterprise applications include AI agents by end of 2026. Retailers using AI/ML experienced 2.3x growth in sales vs. non-adopters (McKinsey). The retailer that controls its own AI stack controls its own competitive destiny.

BUSINESS IMPACT

• Walmart is now selling its AI logistics technology as SaaS to other retailers — turning competitive advantage into a revenue line (IT Brew, December 2025)

• 67% of retail executives expect AI-driven personalization capabilities within the next year (Deloitte Global 2026)

• GenAI ROI: improved time efficiency (49%) and cost efficiency (40%) across enterprise deployments (Gartner 2025)

• The gap between AI-native retailers and laggards is widening at an accelerating rate — early movers are building proprietary compounding data advantages

STRATEGIC IMPLICATIONS

• Stop piloting generic AI. Build or license retail-specific LLMs trained on your own transaction, behavioral, and operational data

• Define the four agent domains every major retailer needs: customer experience, associate empowerment, supplier management, developer ecosystem

• Make AI investment accountability structural: assign a C-level owner who reports directly to the CEO with board-level visibility

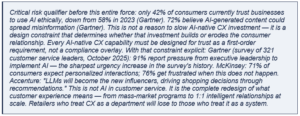

Trend #3 — Conversational & Multimodal Commerce: The Search Bar Is Dead

WHY THIS EXISTS

58% of shoppers already use generative AI tools instead of traditional search engines for product recommendations (Capgemini 2025). 43% of Gen Z now begin product searches on TikTok or social platforms rather than Google or Amazon (Akeneo). Adobe reports 1,950% YoY increase in retail site traffic from chat interactions during 2024 Cyber Monday. Accenture: “Identifying how to best link LLMs to a retailer’s product and brand information will be key to whether a brand’s product appears as a recommendation.”

BUSINESS IMPACT

• SEO and paid search strategies built around keywords become structurally less effective — the algorithm now reads your product data, not your page rank

• Retailers with the richest, most accurate product data win the AI recommendation; those with poor data are invisible in the AI commerce layer

• Visual search (image-to-product), voice reordering (smart speakers, connected cars), and ambient computing are creating new purchase channels that most retailers have no presence in

STRATEGIC IMPLICATIONS

• Audit product data quality end-to-end against AI readability standards — the AI agent reads every attribute, every image, every review

• Develop conversational commerce capability inside your own apps, not just through third-party AI platforms — own the conversational relationship or it will be owned for you

• Treat your product catalog as a strategic AI training asset: richness, accuracy, and real-time accuracy are now competitive differentiators

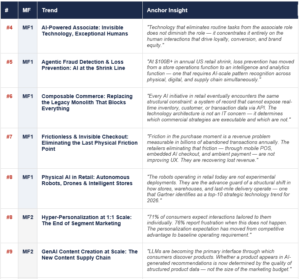

Trend #4 — AI-Powered Associate: Invisible Technology, Exceptional Humans

WHY THIS EXISTS

NRF 2026 consensus from LVMH, Dick’s Sporting Goods, Ulta Beauty, and Abercrombie & Fitch: the industry is moving from clunky legacy customer service into frictionless integration where technology retreats into the background. When an associate can check global inventory, personalize a recommendation, and process a transaction from an iPhone without glitches — the technology has successfully retreated. Ed Stack (Dick’s Sporting Goods): “Yes, if” mindset — AI eliminates every “No, because the system is down.” Microsoft NRF 2026: AI agents making data-driven decisions, optimizing operations, and automating routine tasks to enhance associate productivity.

BUSINESS IMPACT

• Associates shift from transaction facilitators to brand ambassadors — measurably improving NPS, basket size, and loyalty

• Mobile-first architecture enables stores to simultaneously serve as fulfilllment hubs, media environments, and experience destinations

• Frontline workforce retention improves when roles are meaningful — associates empowered to deliver excellent service are more engaged than those processing transactions

• Abercrombie & Fitch CEO Fran Horowitz (NRF 2026 Visionary Award): “Retail is a journey. There’s no finish line. Everything continues to evolve.”

STRATEGIC IMPLICATIONS

• Move the entire store’s capability onto mobile-first architecture — replace fixed POS terminals with associate devices that provide real-time access to global inventory, customer history, and personalized recommendations

• Redefine associate performance metrics: shift from transactions-per-hour to NPS, basket conversion, and service quality

• Design the associate workflow before selecting the technology — the tool should serve the role, not define it

Trend #5 — Agentic Fraud Detection & Loss Prevention: AI at the Shrink Line

WHY THIS EXISTS

US retail shrink exceeded $100B annually. 837 retail cybersecurity incidents in 2024 with 419 confirmed data disclosures (Verizon DBIR 2025). Ahold Delhaize’s systems were disrupted by a third-party breach — cited in the NRF Top 50 2025 report. The attack pattern is instructive: the target was not the retailer’s core systems but a third-party provider integration. As retailers connect to UCP, hyperscaler platforms, payment providers, logistics APIs, and retail media networks, every integration is a potential attack vector. Gartner: 70% of retail operators will adopt AI-based cybersecurity by 2026. IDC: 50% of CIOs are diversifying security strategies to counter new supply chain and GenAI-specific risks. PCI DSS v4.0 compliance requirements (2025 deadlines) are forcing security investment regardless of shrink strategy.

BUSINESS IMPACT

• AI-powered behavioral analytics detect organized retail crime patterns — group coordination, return abuse patterns, and employee theft signals — invisible to human security teams

• Return fraud intelligence identifies abuse patterns across channels and geographies, directly protecting margin in the highest-cost return categories

• Cyberattack on retail supply chain partner is now a top-5 operational risk — third-party security is no longer optional

STRATEGIC IMPLICATIONS

• Deploy AI-driven loss prevention across the full shrink perimeter: physical store, digital commerce, and supply chain simultaneously — siloed approaches miss cross-channel fraud patterns

• Integrate cybersecurity into the retail tech stack as an embedded design requirement, not a compliance add-on

• Package fraud and identity intelligence as commercial products: identity verification and network-based fraud detection have enterprise B2B revenue potential

Trend #6 — Composable Commerce: Replacing the Legacy Monolith That Blocks Everything

WHY THIS EXISTS

Gartner: majority adoption of composable commerce (MACH: Microservices, API-first, Cloud-native, Headless) by 2027. Every trend in this analysis — UCP integration, AI super-agents, conversational commerce, dark store inventory, retail media, embedded payments — requires composable architecture as a prerequisite. Gartner: composable BSS reduces deployment timelines by 50%. 65.5% of Digital Commerce 360 Top 1,000 retailers show in-store stock status online — a basic capability that still requires unified inventory as a foundation.

BUSINESS IMPACT

• Legacy monoliths are the single most common hidden reason AI initiatives fail — the data is fragmented, the APIs do not exist, the real-time feeds are not built

• Composable architecture enables UCP integration, AI agent access, retail media monetization, and unified commerce in ways legacy systems structurally cannot

• The investment required for MACH migration is significant — but the cost of not migrating is compounding at the rate of every AI initiative that fails on legacy infrastructure

STRATEGIC IMPLICATIONS

• Treat legacy platform retirement as a CEO-level strategic priority with board visibility — not an IT modernization program with an IT budget

• Build toward MACH architecture in phases: unified inventory and OMS first (they block the most other initiatives), then composable checkout, then personalization layer

• Map every AI initiative to the architectural prerequisite it requires — most will be blocked by the same legacy constraint, and naming it explicitly is the first step to fixing it

Trend #7 — Frictionless & Invisible Checkout: Eliminating the Last Physical Friction Point

“Friction in the purchase moment is a revenue problem measurable in billions of abandoned transactions annually. The retailers eliminating that friction — through mobile POS, embedded AI checkout, and ambient payment — are not improving UX. They are recovering lost revenue.”

WHY THIS EXISTS

NRF 2026 / Payplug analysis: eliminating the fixed checkout counter is the stated 2026 goal for leading retailers. US BOPIS reached $132.8B in 2024, growing at 16.7% CAGR through 2030 — proving consumers want format flexibility over fixed checkout. SoftPOS (every associate becomes a mobile POS on a standard smartphone) is the bridge technology. Amazon removed “Just Walk Out” from US Fresh stores in favor of smart carts with better unit economics — demonstrating that frictionless checkout is evolving, not reversing.

BUSINESS IMPACT

• Friction at checkout is the single biggest driver of cart abandonment — billions in annual lost revenue across physical and digital channels

• SoftPOS converts every associate into a checkout terminal, eliminating queue costs and enabling floor-based service selling without fixed infrastructure

• Invisible checkout inside UCP (Trend 1) enables purchase completion without visiting a retailer’s website — the checkout becomes part of the AI conversation

STRATEGIC IMPLICATIONS

• Set elimination of fixed checkout counters as a public strategic milestone — the commitment signals organizational change, not just technology deployment

• Deploy SoftPOS across associate devices as the bridge technology between today’s fixed format and tomorrow’s invisible payment

• Integrate checkout capability into UCP and AI commerce flows — the checkout should be invisible inside the purchase journey, not a separate step

Trend #8 — Physical AI in Retail: Autonomous Robots, Drones & Intelligent Stores

“The robots operating in retail today are not experimental deployments. They are the advance guard of a structural shift in how stores, warehouses, and last-mile delivery operate — one that Gartner identifies as a top-10 strategic technology trend for 2026.”

WHY THIS EXISTS

Gartner named Physical AI — AI that perceives, decides, and acts in the physical world — a top strategic technology trend for 2026. In retail this manifests as: autonomous shelf-scanning robots (Simbe Robotics deployed across hundreds of stores including BJ’s Wholesale); Brain Corp autonomous floor-cleaning and analytics robots (operating in 13,000+ retail locations globally); computer vision at self-checkout eliminating cashier error; and drone delivery expanding from pilot to commercial scale. The enabling infrastructure layer beneath Physical AI that most retail programs underestimate is edge computing: AI inference must happen at the store level — on local servers, not via cloud roundtrip — to achieve the sub-100ms response times that loss prevention, real-time inventory, and checkout systems require. IDC research director Margot Juros (IDC Retail Insights) explicitly identifies edge computing as a critical gap in retail AI strategies: “Modernized infrastructure strategies utilizing cloud, edge technologies and advanced networking support the need for real-time data access and processing essential for many AI applications.” Werner Vogels’ 2026 predictions explicitly emphasize distributed computing closer to the point of data generation. Walmart Wing drone delivery serves 160+ US locations. Amazon Prime Air is scaling. Forward horizon: Amazon CTO Werner Vogels named quantum-safe cryptography as a top 2026 technology priority. As quantum computing advances, current encryption standards protecting payment data, customer data, and supply chain data will become vulnerable within 3-5 years. Retail holds some of the highest volumes of sensitive transactional data in any industry. Quantum-resistant cryptography planning is not a 2030 concern — it is a 2026 architectural decision that will determine data security posture for the decade ahead.

BUSINESS IMPACT

• Autonomous shelf-scanning robots reduce out-of-stock rates by up to 30% while eliminating the associate labor required for manual inventory counts — directly improving both margin and customer experience

• Physical AI in the store creates a data collection infrastructure that no manual process can replicate: real-time shelf-level inventory, traffic flow patterns, conversion data by fixture, and customer interaction mapping

• The economics of in-store physical AI are improving rapidly: early deployments required significant capex with 3-5 year payback; current-generation systems reach payback in 12-18 months at mid-market retailer scale

STRATEGIC IMPLICATIONS

• Audit the in-store tasks currently absorbing associate time that physical AI systems can handle more accurately and continuously: shelf scanning, floor cleaning, security monitoring, and basic customer wayfinding are the established entry points

• Evaluate drone delivery as a last-mile strategy for your highest-density urban markets — Wing, Amazon Air, and Zipline are available as infrastructure partners; the capital is not required upfront

• Build the sensor infrastructure before committing to specific physical AI applications — the data generated by in-store sensors is a strategic asset independent of the specific robots operating on that infrastructure

Meta-Force 2: AI-Native Customer Experience & Product Innovation

Trend Summary

Trend Deep-Dives

Trend #8 — Hyper-Personalization at 1:1 Scale: The End of Segment Marketing

WHY THIS EXISTS

McKinsey: 71% of consumers expect personalized interactions, 76% frustrated when it does not happen. Costco tied AI-powered recommendation carousels to $470M in e-commerce sales in a single quarter (Q2 FY2026, per CFO Gary Millerchip). Klarna’s GenAI assistant handled the equivalent workload of 700 full-time agents in its first month. E-commerce conversion rate improvement: up to 30% with AI chatbots (Gartner). Over 70% of US digital retailers believe AI-driven personalization will affect their business more than any other factor (Bolt/EMARKETER). Companies with AI-led processes are 1.8x more likely to achieve double ROI (Accenture).

BUSINESS IMPACT

• Segment-based marketing (target the 25–34 year-old urban professional) is being replaced by 1:1 real-time personalization that adjusts every interaction based on live behavioral signals

• The conversion rate improvement from AI personalization (up to 30%) dwarfs anything achievable through traditional segmentation or A/B testing

• Retailers without a Customer Data Platform (CDP) unifying behavioral, transactional, and contextual data cannot run genuine 1:1 personalization — the data foundation is the prerequisite

STRATEGIC IMPLICATIONS

• Build the CDP foundation first — a unified customer identity that merges purchase history, behavioral signals, location context, and real-time events into a single governed profile

• Shift marketing org from campaign-based to always-on AI-driven engagement — the campaigns should be the exception, individual-level real-time response should be the norm

• Measure personalization in commercial terms: conversion rate lift, ARPU improvement, churn reduction — not engagement metrics or click-through rates

Trend #9 — GenAI Content Creation at Scale: The New Content Supply Chain

WHY THIS EXISTS

Accenture: “LLMs will become the new influencers, driving shopping decisions through recommendations — identifying how to best link LLMs to a retailer’s product and brand information will be key to whether a brand’s product appears as a recommendation.” Adobe: 693% surge in GenAI holiday traffic. GenAI is enabling retailers to generate product descriptions, marketing copy, imagery, and video at a fraction of the previous cost — but the quality and accuracy of AI-generated content directly determines AI agent recommendation probability.

BUSINESS IMPACT

• AI-generated product content that is accurate, rich, and structured will rank higher in AI recommendations than sparse, human-written legacy descriptions

• The content supply chain for retail has fundamentally changed — AI can generate 10,000 product descriptions in the time it took to write 10 manually, at quality levels that equal or exceed human output

• Brand voice consistency across AI-generated content requires explicit brand model training — without it, GenAI produces generic, interchangeable content that commoditizes the brand

STRATEGIC IMPLICATIONS

• Audit product catalog for AI readability: structured attributes, accurate descriptions, rich imagery, real-time pricing — and treat this as a commercial priority, not a content team task

• Develop a GenAI content strategy with explicit brand voice guidelines, quality validation, and human-in-the-loop review for brand-critical content

• Invest in the infrastructure to keep AI-generated content accurate and current — stale or inaccurate AI content is worse than no AI content

Trend #10 — AR/VR Virtual Try-On & Immersive Commerce: The Physical-Digital Collapse

WHY THIS EXISTS

Global same-day delivery market projected to exceed $330B by 2032. BOPIS/BORIS (Buy Online Return In Store) defining the blended format. IKEA Kreativ: AI-based room scanning and virtual design — customers can redesign their bedroom from their sofa and add all products to cart automatically. Sephora Virtual Artist: virtual makeup try-on removed the trial barrier for online beauty purchases. Nike AI-powered fitting rooms. Global immersive commerce growing. Adobe reports “hyper-personalization in retail driving measurable revenue lift.”

BUSINESS IMPACT

• Virtual try-on eliminates the #1 reason consumers do not purchase online: inability to assess fit, size, or how a product looks in their space

• Returns rates for categories with effective AR try-on drop significantly — directly improving margin on a structural basis

• Immersive commerce creates differentiated shopping experiences that social platforms and pure e-commerce cannot replicate — the physical-digital boundary has collapsed

STRATEGIC IMPLICATIONS

• Identify the top return-driving categories in your assortment and build AR try-on capability starting there — the ROI case is returns reduction, not just conversion improvement

• Integrate virtual try-on into both digital channels and physical stores — the physical store becomes the most powerful AR platform when combined with digital inventory

• Treat immersive commerce as a long-term brand asset, not a technology demonstration — the retailers who build this capability in 2026 will have a structural advantage by 2028

Trend #11 — AI-Powered Loyalty Reinvention: From Points to Predictive Intelligence

WHY THIS EXISTS

Gartner analyst Kate Muhl: “In recessionary times, consumers are about self-protection and not spending — getting as much value as you can for your dollar.” Customers are willing to share data if it results in more personalized and rewarding experiences — 67% willing to share data for personalized experiences (Press Ganey Forsta). Costco: AI-powered recommendation carousels drove $470M in e-commerce sales in Q2 FY2026. Traditional loyalty programs have minimal impact on GenZ loyalty — which is values-based, not points-based. Gartner: 51% of customers willing to use GenAI assistant for service interactions.

BUSINESS IMPACT

• Points-based loyalty programs are being disrupted from both sides: GenZ does not respond to them, and AI can deliver value without a formal program through anticipatory personalization

• Retailers with CDP infrastructure can deliver personalization-as-loyalty: remembering preferences, anticipating needs, and proactively surfacing relevant offers — without requiring a program enrolllment

• Predictive loyalty uses behavioral signals to identify at-risk customers before they churn, enabling proactive intervention that traditional programs cannot execute at speed or scale

STRATEGIC IMPLICATIONS

• Audit your loyalty program against GenZ behavioral patterns: are the rewards relevant, the communication non-intrusive, the values alignment genuine?

• Build predictive churn detection into your loyalty infrastructure — identify customers showing disengagement signals 30–60 days before they leave

• Design loyalty around three axes: transactional value (savings), experiential value (access, exclusivity), and values alignment (sustainability, community) — the retailers winning GenZ loyalty address all three

Trend #12 — Conversational AI Service at Scale: The 700 FTE Equivalent Moment

WHY THIS EXISTS

Gartner survey (321 customer service leaders, October 2025): 91% report pressure from executive leadership to implement AI — marking a sharp increase in urgency. Klarna’s GenAI-powered assistant handled the equivalent workload of 700 full-time agents in its first month. Gartner: projected $80B in contact center labor cost savings by 2026. 51% of customers willing to use a GenAI assistant for service interactions (Gartner), but 49% prefer alternatives — the design of escalation paths is as important as the AI itself.

BUSINESS IMPACT

• The cost differential between AI and human service interactions (12x according to industry data) creates an irresistible efficiency case — but poor implementation creates brand damage that exceeds the cost savings

• First-contact resolution is the key metric: AI must solve the problem, not create a frustrating loop that ends in human escalation — poor AI service is worse than no AI service

• Human agents become the strategic asset in an AI service world: they handle complex, emotional, and brand-critical interactions that AI cannot — the role transformation is as important as the technology deployment

STRATEGIC IMPLICATIONS

• Design the service journey before deploying AI — map which interactions AI handles fully, which it assists, and which immediately escalate to humans

• Ensure clear, frictionless escalation paths from AI to human agents — 49% of customers prefer human interaction, and forcing them through AI damages the relationship

• Measure AI service quality in customer terms: first-contact resolution rate, customer effort score, NPS — not just cost-per-interaction

Trend #13 — Voice, Ambient & Neural Commerce: The Zero-Click Purchase Economy

WHY THIS EXISTS

Connected cars enabling drive-thru voice orders. Smart speakers reordering household staples. IoT-enabled automatic replenishment (Amazon Dash evolved into ambient reorder). 43% of GenZ begin product searches on TikTok or social platforms. OpenAI’s Instant Checkout feature lets users purchase without leaving ChatGPT. Gartner: 40% of enterprise applications will include task-specific AI agents by end of 2026 — many of these are consumer-facing. Neural commerce: AI that anticipates purchase needs before the consumer is aware of them.

BUSINESS IMPACT

• Zero-click purchasing is real and growing — AI agents completing purchases on behalf of consumers represents a new channel that most retailers have no presence in

• Ambient commerce (smart home reordering, connected car purchasing) creates subscription-like revenue without requiring a formal subscription — continuous, low-friction replenishment

• The retailer that is not programmatically discoverable through voice and ambient interfaces will be invisible to a growing segment of purchase occasions — particularly for FMCG, household staples, and routine replenishment

STRATEGIC IMPLICATIONS

• Audit your product assortment for ambient commerce suitability: high-frequency, low-decision-complexity SKUs are the first targets for automated reordering

• Build the API infrastructure that allows AI agents and smart devices to query your inventory, pricing, and delivery capability in real time

• Develop a voice commerce strategy starting with existing smart speaker platforms — Alexa skills, Google Actions — before the channel consolidates around a single dominant platform

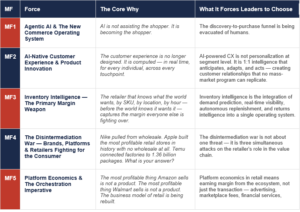

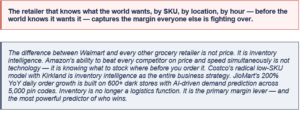

Meta-Force 3: Inventory Intelligence — The Primary Margin Weapon

Trend Summary

Trend Deep-Dives

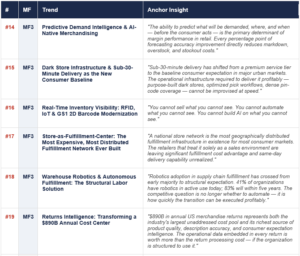

Trend #14 — Predictive Demand Intelligence & AI-Native Merchandising

WHY THIS EXISTS

McKinsey: GenAI could create $240–390B in value for retail (approximately +1.2–1.9pp margin uplift) via smarter merchandising, marketing, and supply chain. Walmart’s Marty (supplier super-agent) automates procurement and inventory optimization at scale. McKinsey NRF 2026: “Agentic-AI-empowered merchants will spend less time reporting and more time strategizing.” Gartner: AI improves demand forecasting through dynamic segmentation and machine learning. Invert the data: retailers using AI/ML solutions experienced 2.3x growth in sales vs. non-adopters (McKinsey).

BUSINESS IMPACT

• 100–200 bps EBIT improvement is realistic with workflow redesign around AI demand intelligence — this is the largest untapped margin pool in retail for most operators (McKinsey)

• Markdown elimination: AI dynamic clearance prevents the promotional cycle that destroys margin by 3–5% of revenue in fashion and seasonal categories

• Personalized assortment by store: right products in the right location vs. uniform national planogram — the 10–15% inventory efficiency gain is the equivalent of adding a fulfilllment center

STRATEGIC IMPLICATIONS

• Build the demand intelligence foundation: unified data across POS, digital behavior, social signals, weather, and external demand signals in a single real-time operating layer

• Redesign the merchandising workflow around AI recommendation — humans own category strategy and brand relationships; AI owns execution, replenishment, and optimization

• Measure forecasting accuracy by SKU, by location, by week — and make it an executive KPI with the same visibility as revenue

Trend #15 — Dark Store Infrastructure & Sub-30-Minute Delivery as the New Consumer Baseline

WHY THIS EXISTS

JioMart: 600+ dark stores, 42% QoQ growth, 200% YoY daily order growth, 5,000 pin codes, 1,000+ cities (Reliance Retail earnings, October 2025). JioMart extended 30-minute delivery to electronics in 10 cities. McKinsey: 65% of US consumers willing to pay extra for two-hour delivery despite trading down on product price. Blinkit, Swiggy Instamart, Getir, and Gorillas have normalized the sub-30-minute model globally.

BUSINESS IMPACT

• Sub-30-minute delivery is becoming the baseline expectation in urban markets worldwide — not the premium tier

• Dark store achieves 3–5x pick efficiency vs. traditional store fulfilllment — the unit economics are structurally different from store-pick models

• JioMart model converts existing retail stores into dark store nodes — converting existing real estate into fulfilllment infrastructure at minimal incremental capex

STRATEGIC IMPLICATIONS

• Map your urban coverage vs. consumer delivery expectations — identify the specific geographies where the dark store gap creates competitive exposure

• Evaluate existing store network as micro-fulfilllment nodes before building dedicated dark stores — the JioMart O2O model is the playbook for converting existing real estate

• Use dark stores as an inventory intelligence asset: concentrated SKU data creates demand visibility impossible at distributed store level

Trend #16 — Real-Time Inventory Visibility: RFID, IoT & GS1 2D Barcode Modernization

WHY THIS EXISTS

Accenture: ~93% of North American retailers use RFID (2025) — yet inventory accuracy at 65–70% remains the industry norm. GS1 “Sunrise 2027”: all POS systems worldwide must scan GS1-powered 2D barcodes by end-2027. EU Digital Product Passports require product-level data traceability that only 2D code infrastructure can deliver. The GS1 mandate is not optional for any retailer with EU shelf presence.

BUSINESS IMPACT

• Inventory accuracy improvement from 65–70% (legacy) to 95%+ (RFID-enabled) — every percentage point is revenue that was previously invisible

• GS1 2D migration generates richer product data at POS: batch numbers, expiry dates, nutritional data, sustainability credentials — the infrastructure for Digital Product Passport compliance

• Real-time shelf visibility enables autonomous replenishment and eliminates manual stock checks — directly reducing the labor cost of inventory management

STRATEGIC IMPLICATIONS

• Accelerate RFID deployment to full store coverage — item-level visibility is the prerequisite for AI demand intelligence, autonomous replenishment, and loss prevention

• Begin GS1 2D barcode migration planning now — Sunrise 2027 deadline is non-negotiable and the transition complexity for large assortments requires 12–18 months of preparation

• Build the data architecture to capture and use the richer product data that 2D barcodes generate — this is the same infrastructure required for EU Digital Product Passport compliance

Trend #17 — Store-as-Fulfilllment-Center: The Most Expensive, Most Distributed Fulfilllment Network Ever Built

WHY THIS EXISTS

US click-and-collect (BOPIS) reached $132.8B in 2024 — approximately 9.9% of e-commerce — growing at 16.7% CAGR through 2030. During peak 2024 holidays, curbside hit 17.5% of online orders — 37% on December 23 (Capital One Shopping). Walmart’s fulfilllment model revamp is specifically cited as a primary reason for its continued NRF #1 global ranking. Home Depot is widely regarded as best-in-class omnichannel integration, using stores as fulfilllment nodes for Pro customer same-day delivery.

BUSINESS IMPACT

• Ship-from-store reduces last-mile delivery cost vs. centralized fulfilllment in most urban markets by 30–40% — the existing real estate asset is the competitive advantage

• BOPIS customers have higher basket sizes than pure e-commerce customers — the pick-up occasion drives incremental attachment purchase

• Same-day delivery becomes operationally viable at scale only with store-as-node architecture — the national fulfilllment center cannot physically deliver in 2 hours

STRATEGIC IMPLICATIONS

• Retrofit existing stores as fulfilllment nodes: dedicated pick areas, optimized backroom layout, associate fulfilllment workflows separate from service workflows

• Invest in unified OMS treating store inventory and warehouse inventory as a single pool — the customer should never know or care where their order originates

• Measure fulfilllment performance by store: fill rate, pick accuracy, cycle time — not just sales per square foot

Trend #18 — Warehouse Robotics & Autonomous Fulfilllment: The Structural Labor Solution

WHY THIS EXISTS

MHI/Deloitte 2025: 41% of supply chain organizations report robotics/automation in use today, rising to approximately 83% within five years. Walmart+Symbotic partnership for warehouse robots. Amazon: 750,000+ robots deployed across the global fulfilllment network. Accenture: combining automation and autonomy reduces order lead times by 27% and increases delivery reliability by 5%.

BUSINESS IMPACT

• Labor cost per unit fulfillled reduces 30–40% in fully automated fulfilllment centers — at scale, this is the most significant cost structure change available to retailers

• 24/7 autonomous operation enables same-day economics that manual fulfilllment cannot achieve — robots do not take breaks, call in sick, or require overtime

• Immigration policy uncertainty and demographic labor supply constraints make robotics not just economically attractive but strategically necessary — Deloitte 2026 explicitly flags this as a retail labor risk

STRATEGIC IMPLICATIONS

• Develop a robotics integration roadmap starting with highest-volume, most repetitive fulfilllment tasks — the ROI case builds fastest at scale

• Follow Walmart’s build/buy model: build core AI fulfilllment intelligence in-house for proprietary advantage; buy specialized robotics from partners for best-of-breed execution

• Design new fulfilllment centers around robotics from the start — retrofitting legacy warehouses for robotics is 3–4x more expensive than designing for automation from day one

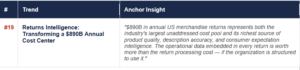

Trend #19 — Returns Intelligence: Transforming a $890B Annual Cost Center

WHY THIS EXISTS

US merchandise returns exceeded $890B annually. NRF 2026 launched NRF Rev — a dedicated event for returns, reverse logistics, and circular retail (January 11–12, 2026, Sheraton Times Square) — signaling returns have reached board-level strategic priority. Return fraud is a significant and growing component of total shrink. Retailers with returns intelligence are identifying product quality issues and customer expectation mismatches weeks before they scale into full return waves.

BUSINESS IMPACT

• 1% reduction in return rate on $1B revenue = $10M in recovered margin — for large retailers, returns intelligence is the largest untapped margin improvement available

• Returns analytics identifies root causes: product quality issues, sizing problems, description inaccuracies, expectation gaps — and enables fixes before the next season

• Integration of returns into recommerce platforms converts cost into revenue: returned items that cannot be restocked at full price become resale inventory

STRATEGIC IMPLICATIONS

• Build returns analytics capability: why is each SKU being returned, by whom, from which channel, with which complaint — this data is the product improvement roadmap

• Design product and customer experience interventions at the root cause: fix the size guide, improve the product description, adjust the imagery — not just improve the returns process

• Integrate recommerce into the returns flow from day one — every returned item should have a defined path: restock, repack, resale, or recycle

Meta-Force 4: The Disintermediation War — Brands, Platforms & Retailers Fighting for the Consumer

Trend Summary

Trend Deep-Dives

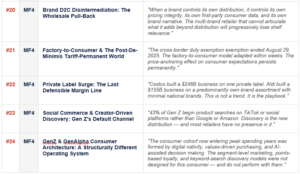

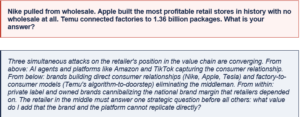

Trend #20 — Brand D2C Disintermediation: The Wholesale Pull-Back

WHY THIS EXISTS

Nike’s wholesale pull-back is the canonical case — reducing wholesale partners to own the customer relationship, then partially reversing when direct growth disappointed at scale. Apple Stores are among the highest revenue-per-square-foot retail operations in the world with zero wholesale. Tesla’s zero-dealership model. Under Armour’s DTC push. The structural driver is consistent: brands that control distribution control price integrity, customer data, and brand experience.

BUSINESS IMPACT

• Multi-brand retailers losing anchor brands face traffic decline and diminished category authority — the loss of Nike from a sports retailer is both a revenue and a traffic event

• Target’s private label ($30B+ annual revenue) is the strategic response: if brands leave, own-brand fills the gap — and at higher margin

• Wholesale dependency creates existential vulnerability — retailers with more than 20% of revenue from any single brand face catastrophic risk if that brand goes DTC

STRATEGIC IMPLICATIONS

• Audit brand concentration risk across your portfolio: which brands could credibly go DTC, what is the revenue impact, and what is your response plan?

• Build the value proposition brands cannot replicate: curation expertise, consumer discovery, physical experience, consumer data sharing, and co-created exclusive product

• Accelerate private label development in the categories where brand pull-back risk is highest — the margin argument makes private label attractive independent of brand risk

Trend #21 — Factory-to-Consumer & The Post-De-Minimis Tariff-Permanent World

WHY THIS EXISTS

De minimis use grew from 134M shipments in 2015 to 1.36B in 2024. The exemption officially ended August 29, 2025. Temu US DAUs fell approximately 48% in May 2025 — then adapted rapidly: US warehouses, American seller onboarding, resumed shipments within weeks. Deborah Weinswig (Coresight): “Don’t count them out. These Chinese e-commerce apps are very adept and agile. I wouldn’t be surprised if the competitiveness gap actually continues to widen.” A July 2025 bill will end cross-border duty exemption for ALL countries by 2027. The factory-to-consumer model is not a cross-border duty exemption story. It is a structural supply chain innovation that permanently reset consumer price expectations.

BUSINESS IMPACT

• The price-anchoring effect of Temu and Shein persists even after cross-border duty exemption — consumers have internalized the price points and will evaluate every purchase against them

• US domestic retailers gain competitive relief on tariff parity — but this only matters if they also compete on speed, convenience, and experience, not just price

• The post-cross-border exemption, high-tariff-permanent world requires retailers to model their competitive position against localized factory-to-consumer players — Temu and Shein are building US warehouse infrastructure

STRATEGIC IMPLICATIONS

• Model the long-term competitive scenario: Temu with 2–3 day US delivery from US warehouse inventory — if this happens, what is your price, speed, and experience response?

• Do not assume tariff protection creates permanent pricing parity — assume the most capable factory-to-consumer operators will adapt and compete; design your strategy around that scenario

• Evaluate your supply chain’s ability to respond to the same speed and flexibility that factory-to-consumer models deliver — demand sensing, rapid replenishment, and zero-inventory production models are available through B2B partnerships

Trend #22 — Private Label Surge: The Last Defensible Margin Line

WHY THIS EXISTS

Target’s private labels generate over $30B in annual revenue. Some grocery retailers see private label constitute over 50% of total product count. Costco’s Kirkland Signature drives 92.1% renewal in North America, 89.7% globally. Aldi’s business model is built on a predominantly own-brand assortment — typically 75–90% depending on market — at $155B global revenue. Tariff-driven cost increases hit national brands proportionally harder — accelerating private label’s price competitiveness. NielsenIQ: private-label products saw record success in 2023, trend accelerating through 2025–2026.

BUSINESS IMPACT

• Private label margin is typically 30–40% higher than equivalent national brand categories — the margin argument for private label investment is now unambiguous

• Tariff-driven cost increases hit national brands harder than own-label — widening the competitive price gap and accelerating consumer trading down to private label

• Kirkland Signature is Costco’s #1 loyalty driver — customers renew their $65 membership specifically to access it, demonstrating that private label can be a premium brand, not just a cheap alternative

STRATEGIC IMPLICATIONS

• Accelerate private label development in the categories most exposed to tariff-driven price inflation — this is both a margin and a competitive defense strategy

• Invest in private label quality and brand identity: consumers willing to pay 9.7% more for sustainable products will pay premium for quality own-brand that delivers genuine value

• Treat private label as a strategic portfolio requiring brand management, product development, and supply chain investment — not as a cost-reduction tactic.

Trend #23 — Social Commerce & Creator-Driven Discovery: Gen Z’s Default Channel

“43% of Gen Z begin product searches on TikTok or social platforms rather than Google or Amazon. Discovery is the new distribution — and most retailers have no presence in it.”

WHY THIS EXISTS

US social commerce sales projected to exceed $100B in 2026. TikTok Shop growing at rates that alarm both Amazon and Walmart. McKinsey: $80B in US social commerce by 2025. Global influencer marketing spend projected at $32.5B. Live commerce delivering 10–30% conversion rates — far higher than traditional e-commerce. User-generated content continues to outperform brand-led messaging.

BUSINESS IMPACT

• Social commerce requires fundamentally different product storytelling: video-first, creator-native, authenticity-driven — the traditional brand campaign model is structurally less effective

• Brands with strong creator ecosystems gain distribution advantages that paid search cannot replicate and that no amount of SEO investment can compensate for

• The social commerce conversion rates (10–30% for live commerce) are not achievable through any other digital channel — the economics are compelling for brands willing to invest in the creator model

STRATEGIC IMPLICATIONS

• Build creator commerce as a distribution channel, not influencer marketing as a tactic — the difference is ownership of the relationship, the content strategy, and the commercial terms

• Develop social-native product storytelling capability: short video, live commerce, shoppable content — these require different skills than traditional marketing teams have

• Measure social commerce as a distinct channel with distinct attribution and distinct economics — not as a subset of digital advertising

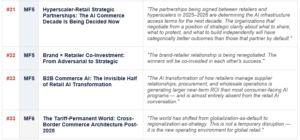

Trend #24 — GenZ & GenAlpha Consumer Architecture: A Structurally Different Operating System

“The consumer cohort now entering peak spending years was formed by digital nativity, values-driven purchasing, and AI-assisted decision making. The segment-level marketing, points-based loyalty, and keyword-search discovery models were not designed for this consumer — and do not perform with them.”

WHY THIS EXISTS

NRF 2026 explicitly called this out: GenZ and GenAlpha “are changing society and shaping future trends at a blinding pace.” 32% of GenZ use their smartphone to find new products while browsing in-store shelves. Myntra (India) hitting 200M annual active users — 50% GenZ. 43% of GenZ begin product searches on TikTok. GenZ loyalty is values-based, not points-based. Abercrombie & Fitch CEO (NRF 2026 Visionary Award): “Retail is a journey. There’s no finish line.”

BUSINESS IMPACT

• Traditional loyalty programs have minimal impact on GenZ loyalty — building a points program to retain GenZ is solving the wrong problem

• GenZ uses AI agents to find deals and compare prices — accelerating both agentic commerce (Trend 1) and factory-to-consumer price pressure (Trend 21)

• Seamless omnichannel is the GenZ baseline expectation, not a differentiator — friction at any touchpoint is brand damage, not an inconvenience

STRATEGIC IMPLICATIONS

• Redesign loyalty programs from points-based to values-based, experience-based, and community-based — GenZ responds to belonging, purpose, and exclusive access, not cashback

• Build social commerce discovery capability — GenZ does not start their purchase journey on your website or in your app — they discover on TikTok and evaluate on Instagram

• Audit every touchpoint for friction: GenZ abandons immediately where older consumers would tolerate delays, and the abandonment is permanent, not temporary

Trend #25 — Subscription & Membership: The Structural Lock-In That Redefines Retention Economics

“Subscription members spend two to four times more than transactional customers, provide richer behavioral data than any other customer type, and create predictable revenue streams that enable investment decisions impossible on transactional revenue alone.”

WHY THIS EXISTS

Costco: 92.1% membership renewal in North America and 89.7% globally (Q2 FY2026 earnings) — the highest subscription retention rate of any retailer in history. Amazon Prime: the most successful consumer subscription in history — Prime members spend 2–4x more than non-members. Global subscription e-commerce projected to reach $904.2B by 2026 (Forbes). Walmart+: growing as the retail equivalent, bundling delivery, fuel savings, and financial services.

BUSINESS IMPACT

• Subscription revenue is more predictable, higher-margin, and more defensible than transactional revenue — the income statement characteristics are fundamentally different

• Subscription members provide richer behavioral data — every interaction is recorded and attributed, enabling the personalization that drives Costco’s $470M digital personalization impact

• Membership creates a natural premium tier for exclusive products, early access, and differentiated experiences — the member is the most valuable customer in the entire file

STRATEGIC IMPLICATIONS

• Evaluate subscription/membership as a structural business model, not a loyalty tactic — the Costco and Amazon evidence is unambiguous, the question is whether your format and consumer relationship support the model

• Bundle services that increase daily utility: delivery, financial services, streaming, fuel — the stickier the bundle, the higher the renewal and the lower the churn

• Design the membership proposition around recurring value demonstration — the member must feel the value consistently, not just at sign-up

Trend #26 — Recommerce & Resale: The Second Sale as the New Loyalty Program

WHY THIS EXISTS

The resale market is growing 11x faster than traditional retail. Patagonia (Worn Wear), Lululemon (Like New), and REI have launched owned recommerce platforms. NRF 2026 launched NRF Rev — a dedicated event for returns, reverse logistics, and circular retail. Consumers willing to pay 9.7% premium for sustainable products (Zappi 2026). EU Ecodesign Regulation creates the mandatory infrastructure for structured recommerce through Digital Product Passports.

BUSINESS IMPACT

• Recommerce captures margin from products already in the market at zero manufacturing cost — the economics are structurally different from first-sale retail

• Brands that own the secondary market control price integrity across the full product lifecycle — preventing the discount spiral that destroys brand equity in the grey market

• EU Digital Product Passports create the technical infrastructure for structured recommerce — compliance builds the foundation for revenue simultaneously

STRATEGIC IMPLICATIONS

• Develop a recommerce strategy for top product categories starting with highest-value, most durable SKUs — fashion, electronics, and sporting goods have the most developed secondary markets

• Build or partner on resale infrastructure before a third-party marketplace (ThredUp, Poshmark) captures the margin and the customer relationship in your category

• Integrate recommerce into the primary brand experience — not as a separate discount channel, but as evidence of product quality and brand commitment to longevity

Seven Meta-Forces. One Retail Reality.

Part 1: The First Four Forces That Explain Why 2026 Feels Like a Breaking Point

For years, retailers treated disruption as a sequence: e-commerce, mobile, marketplaces, then “AI.” That mental model is now outdated. In 2026, the forces reshaping retail are simultaneous and reinforcing — and they’re changing not just how retail sells, but how retail works. This series introduces the meta-forces behind the change, starting with the four that are already moving fastest.

If you take only one thing from Part 1, take this: retail strategy can no longer be a collection of initiatives. The system is changing. AI is becoming the shopper, experience is becoming computed, inventory is becoming the margin engine, and disintermediation is rewriting who gets to own the consumer.

Next: Part 2 — the forces that decide the new winners: platform economics, geopolitics and regulation, and the value–margin paradox. These are the levers that determine whether you merely survive the reset — or architect advantage through it.

Leave a Reply