Telecom at the Inflection Point: The Battle for Control in the AI Economy

Executive Summary

Over the last 24–36 months, the telecommunications industry has crossed a structural inflection point. This is not another G-cycle upgrade — it is a fundamental reordering of value pools. AI is collapsing cost structures, software is redefining network economics, growth is shifting to ecosystems and verticals, trust and sovereignty are becoming monetizable, and hyperscalers are moving simultaneously up and down the stack.

Telecom is no longer upgrading infrastructure. It is repositioning in the AI economy.

Key Statistics from the Research Corpus

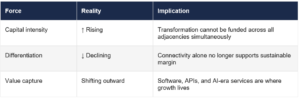

The Core Strategic Tension

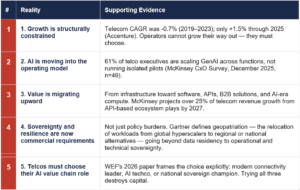

The 5 Structural Realities

Five realities are converging simultaneously and explain why these 40 trends exist:

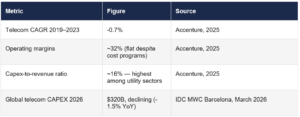

The Financial Forcing Function

This is the context that makes every trend urgent rather than optional:

Master Trend Matrix: All 40 Trends at a Glance

Meta-Force 1: AI-Native Operations & Workforce Leverage

Trend Summary

Trend Deep-Dives

Trend #1 — AI-First Telco Operating Model

THE SHIFT

From human-led workflows and functional automation toward AI-orchestrated decisioning across the full operating model — network, customer, field, finance, and commercial operations running as a unified intelligence system rather than siloed processes.

WHY THIS EXISTS

Explosion in network operational complexity (5G, Open RAN, multi-cloud, IoT scale). Availability of foundation and agentic models capable of autonomous multi-step reasoning. Margin pressure making incremental efficiency programs structurally insufficient. McKinsey CxO Survey (Jan 2026, n=125): 64% of telco leaders expect AI to contribute more than 5% of revenues; 40% anticipate AI-driven cost reductions exceeding 10% at full scale.

BUSINESS IMPACT

- 20–40% opex reduction potential through predictive automation (Gartner/Deloitte)

- Faster MTTR, lower churn, higher NPS across all service lines

- Reduced dependency on institutional knowledge — making the organization less fragile to talent loss

- Only 47% of operators have seen measurable AI impact despite 61% scaling programs (McKinsey) — the gap is operating model, not technology

WHAT LEADERS MUST DO

- Redesign processes end-to-end rather than overlaying AI on existing workflows

- Define explicit human vs. machine decision boundaries and enforce them operationally

- Tie every AI program to hard P&L metrics: opex per site, truck rolls, MTTR, deal velocity

- Fix data foundations first — AI on fragmented data produces confident wrong answers

Trend #2 — Agentic Customer Care and Service Resolution

THE SHIFT

From scripted bots and assisted chat toward reasoning agents that autonomously resolve full customer journeys — handling backend system interactions, complex queries, and multi-step service changes without human escalation.

WHY THIS EXISTS

Only 34% of telecom customers feel satisfied; 70% are frustrated by inconsistent cross-channel experience (WEF). Agentic AI introduced autonomous decision-making into customer operations in 2025 (IDC MWC 2026). Customer care represents 15–20% of telco opex — the largest single addressable cost pool for AI.

BUSINESS IMPACT

- A European telco achieved 40% reduction in service resolution time, 35% improvement in customer effort scores, and 28% increase in digital adoption via AI-powered automation (WEF, 2025)

- Lower cost-to-serve per interaction with higher first-contact resolution rates

- Fewer escalations to human agents, reducing headcount dependency in repetitive resolution work

WHAT LEADERS MUST DO

- Deploy multi-agent orchestration across channels and backend systems — not just front-end chatbots

- Invest in retrieval policies and output checkers to manage hallucination risk in high-stakes service contexts

- Create daily agent scorecards with performance metrics across care, field, and network domains

Trend #3 — Autonomous Network Assurance and Closed-Loop Remediation

THE SHIFT

From human-operated NOCs making reactive decisions toward self-healing, self-optimizing network systems that detect, diagnose, and remediate faults autonomously within governed boundaries.

WHY THIS EXISTS

Gartner projects 30% of CSPs will reach partial network autonomy by 2026. TM Forum data (2025): only 4% of operators self-reported Level 4 autonomous network status; 85% aspire to reach it by 2030 — an extraordinary gap that is the investment thesis. Network operations will consume 50% of total opex by 2027 (WEF).

BUSINESS IMPACT

- Gartner: advanced AIOps platforms can cut incident resolution time by 60%

- Reduction in truck rolls and field dispatch for remotely resolvable issues

- Energy optimization through real-time power management — directly tied to sustainability targets

- Freed operational resources shift from maintenance to innovation

WHAT LEADERS MUST DO

- Invest in closed-loop AI with full telemetry integration across RAN, core, and transport

- Build autonomous network capabilities in layers — assurance first, then optimization, then provisioning

- Address the data quality prerequisite: autonomous remediation fails on inaccurate network inventory

- Publish TM Forum autonomous network level (0–5) as a tracked executive metric

Trend #4 — AI Copilots for Engineering, Planning, and Field Operations

THE SHIFT

From experience-dependent decisions made by scarce senior engineers toward AI-assisted decision-making embedded directly into engineering workflows, capacity planning tools, and field technician interfaces.

WHY THIS EXISTS

IDC projects AI-supporting technology spend rising from $337B in 2025 to $749B by 2028, with two-thirds embedded directly into core operations — field service and network planning are primary targets. Talent scarcity in experienced network engineers creates institutional knowledge risk. Field service costs (truck rolls, site visits) represent 20–30% of opex at most large operators.

BUSINESS IMPACT

- Faster network deployments with fewer configuration errors

- Improved field technician productivity and first-time resolution rates

- Reduced dependency on senior engineering expertise for routine complex decisions

- Accelerated software development cycles — AI coding assistants delivering measurable impact across technical teams (McKinsey, Nov 2025)

WHAT LEADERS MUST DO

- Embed copilots directly into the engineering and field tools engineers already use — not standalone applications

- Define which decisions require human sign-off vs. AI recommendation vs. full AI autonomy

- Create feedback loops so copilot recommendations improve from field outcomes over time

Trend #5 — AI-Driven Workforce Productivity and Knowledge Automation

THE SHIFT

From tacit knowledge locked in experienced individuals toward AI-accessible systems that encode, distribute, and apply institutional expertise across the organization — making the entire workforce more capable, not just more efficient.

WHY THIS EXISTS

Accenture: 76% of CSP executives say they need to upskill or reskill employees in GenAI tools within 3 years. WEF’s 2025 Future of Jobs report flags AI, big data, networks, and cybersecurity as the highest-demand skills in telecom — a market where operators compete with hyperscalers at a structural disadvantage. GenAI delivering ROI through improved time efficiency (49%) and cost efficiency (40%) across enterprise deployments (Gartner, 2025).

BUSINESS IMPACT

- Reduced dependency on senior staff for complex diagnostic and planning tasks

- Faster onboarding of new engineers to productive contribution

- Consistent execution quality across geographies and experience levels

- Workforce evolution is less about headcount cuts and more about redesigning work at scale (IFS/WEF, 2026)

WHAT LEADERS MUST DO

- Codify knowledge into structured, AI-consumable formats — technical runbooks, resolution trees, engineering standards

- Baseline current skill profiles, augment critical roles first, then expand enablement systematically

- Align workforce AI programs with IT/Legal/Privacy — especially where AI accesses sensitive network or customer data

- Integrate AI capability into career paths and continuous learning cycles, not one-off training events

Trend #6 — AI-Led Revenue Assurance, Fraud Analytics & Structural Cost Reset

THE SHIFT

From incremental efficiency programs and reactive fraud management toward fundamental cost base redesign enabled by AI — and the simultaneous opportunity to monetize AI-driven fraud defense as an enterprise product.

WHY THIS EXISTS

Cybercrime costs rising toward $10.5 trillion annually — telcos managing high-value transaction flows are prime targets and prime defenders. Operators have structural access to real-time transaction, identity, and behavioral data that makes telco fraud analytics uniquely valuable to financial services, healthcare, and government buyers. McKinsey: AI driving less than 2% of revenues for over half of operators that have tested AI use cases — the gap signals unrealized structural cost potential.

BUSINESS IMPACT

- Leaner organizations with fewer management layers and lower cost per subscriber

- Revenue assurance improvements directly protect margin — typically 1–3% of revenue recoverable

- Fraud analytics as a monetizable B2B product — identity, SIM fraud, account takeover — creates a new revenue line from existing capabilities

- Financial services, healthcare, and government are willing to pay premium for regulated, auditable fraud intelligence

WHAT LEADERS MUST DO

- Rebaseline cost assumptions structurally, not just annual budgets

- Map the full decision inventory — identify which decisions AI should own vs. support vs. merely inform

- Package fraud and identity intelligence as commercial products for enterprise and government buyers

Meta-Force 2: Programmable, Cloud-Native, Real-Time Network Economics

Trend Summary

Trend Deep-Dives

Trend #7 — Cloud-Native Core and Transport Modernization

THE SHIFT

From hardware-bound, vendor-specific network stacks toward cloud-native, containerized, microservices-based architectures running on commodity infrastructure — enabling continuous delivery, rapid iteration, and genuine vendor flexibility.

WHY THIS EXISTS

IDC documents a structural CAPEX-to-OPEX shift as telcos increasingly rely on ISVs and cloud providers for virtualization and AI. The 5G non-standalone CAPEX peak has passed in high-income markets — freed capital must flow to higher-return software and platform plays (IDC, March 2026). Legacy monolithic stacks cannot support agentic AI, real-time APIs, or composable service delivery.

BUSINESS IMPACT

- Faster scaling without proportional capex investment

- Reduced total cost of ownership through commodity hardware

- Vendor flexibility reduces single-source dependency and improves negotiating leverage

- Prerequisite for every other trend in this meta-force: composable BSS, intent-based automation, network APIs

WHAT LEADERS MUST DO

- Accelerate full-stack cloud-native transformation — not front-end modernization over legacy core

- Treat cloud-native migration as a multi-year architecture program, not an IT project

- Build for portability: avoid cloud-native lock-in that replicates vendor lock-in at the hyperscaler layer

Trend #8 — Open RAN: The Architecture That Changes Everything

THE SHIFT

From proprietary, integrated RAN equipment controlled by Nokia, Ericsson, and Huawei toward open, interoperable software layers running on commodity hardware — breaking the architectural lock that has constrained telecom infrastructure economics for decades.

WHY THIS EXISTS

Dish Network’s all-Open RAN greenfield build and Rakuten’s pioneering deployment in Japan proved commercial viability. Vodafone committed to 30% Open RAN by 2030. Google Distributed Cloud, Azure for Operators, and AWS Wavelength are all built for an Open RAN world. Geopolitical pressure to reduce Huawei dependency has accelerated operator interest in Open RAN as a supply chain diversification strategy.

BUSINESS IMPACT

- Breaks single-vendor lock — operators can mix best-of-breed RAN components

- Enables hyperscaler AI capabilities to be applied directly to RAN optimization

- Creates new integration complexity and security surface area in the transition period

- Foundation for composable BSS, intent-based orchestration, digital twins, AI-driven assurance

WHAT LEADERS MUST DO

- Develop a clear Open RAN migration roadmap — starting with greenfield or legacy replacement sites

- Invest in systems integration capability: Open RAN’s value depends on getting the integration right

- Participate actively in O-RAN Alliance standards — operators shaping standards shape their future costs

Trend #9 — Network APIs as Commercial Products

THE SHIFT

From connectivity sold as a service toward programmable network capabilities exposed as APIs with commercial pricing, SLAs, and developer tooling — creating a new class of revenue from existing infrastructure.

WHY THIS EXISTS

IDC: over 25% of telecom revenue growth will come from API-based monetization by 2027. Deutsche Telekom’s MACE API unit, Telefónica’s NaaS Dynamic Network, and the GSMA Open Gateway initiative are moving this from concept to commercial reality. Hyperscalers built trillion-dollar ecosystems on APIs — telcos are replicating the pattern with network-native capabilities hyperscalers cannot replicate.

BUSINESS IMPACT

- New revenue streams from existing network assets with minimal incremental capex

- Developer ecosystem engagement creates compounding value — third-party applications drive network usage

- Quality-on-Demand, SIM-swap authentication, network slicing, and edge compute become purchasable capabilities

- Risk: avoiding commoditization requires differentiated capabilities, not just API wrappers on commodity connectivity

WHAT LEADERS MUST DO

- Treat APIs as products — with product management, pricing, documentation, SLAs, and developer support

- Address the critical challenge: developers require training and certification — determine who provides this

- Participate in GSMA Open Gateway to ensure cross-operator interoperability — the network effect multiplies value

Trend #10 — Real-Time, Event-Driven Telecom Systems

THE SHIFT

From delayed, batch-processing BSS/OSS systems making decisions on stale data toward instantaneous, event-driven architectures enabling real-time personalization, automation, network response, and AI inference on live operational data.

WHY THIS EXISTS

Agentic AI systems and autonomous network operations require real-time data streams — batch architecture creates a fundamental incompatibility. Network slicing, quality-on-demand, and dynamic pricing all require sub-second response to network conditions. Personalization at scale requires real-time behavioral signals, not overnight batch profiles.

BUSINESS IMPACT

- Enables genuine personalization — not segment-based approximation

- Enables automation that responds to live conditions rather than historical averages

- Improves responsiveness to network events — moving from minutes-to-hours detection toward seconds-to-minutes

- Prerequisite for autonomous assurance, agentic customer care, and intent-based orchestration

WHAT LEADERS MUST DO

- Re-architect core systems to event-driven models — Kafka, Flink, and real-time data platforms are the technical layer

- Identify use cases needing real-time first (network assurance, fraud detection, personalized offers) and sequence migration around them

- Do not attempt to run real-time AI on batch data foundations — fix the architecture before scaling the AI

Trend #11 — Unified Telecom Data Fabric Across OSS, BSS, and Network Domains

THE SHIFT

From fragmented data siloed across OSS, BSS, CRM, network inventory, and field systems toward a unified operational data layer that provides a single source of truth across every operational domain.

WHY THIS EXISTS

IDC EMEA Telco Transformation Survey (July 2025, n=150): interoperability failures and lack of a single source of truth in network data are the top two barriers to both autonomous networks and AI adoption — the same problem, two symptoms. McKinsey: a broad and integrated data foundation is essential to redesign processes end-to-end.

BUSINESS IMPACT

- Without this: AI programs produce locally smart, globally wrong decisions

- Cross-domain visibility enables genuine operational intelligence — predicting failures, correlating customer impact with network events

- Better investment decisions — understanding which network assets actually drive customer experience outcomes

- Network inventory accuracy is the single most common reason autonomous network programs fail

WHAT LEADERS MUST DO

- Create a single operational data model — not a data lake that replicates fragmentation at scale

- Overhaul network inventory systems: inaccurate inventory is the most common autonomous network program failure point

- Treat data unification as a CEO-level strategic priority, not an IT data management program

Trend #12 — Network Slicing and Quality-on-Demand Monetization

THE SHIFT

From best-effort, shared network capacity toward virtualized, dedicated network slices with guaranteed performance parameters — sold to enterprise customers as differentiated service tiers with commercial pricing.

WHY THIS EXISTS

5G Standalone architecture (SA) is the technical enabler — operators that have deployed NSA-only cannot offer true network slicing. Enterprise customers in manufacturing, healthcare, logistics, and automotive require guaranteed latency and bandwidth that shared networks cannot provide. Network slicing creates a natural premium pricing tier that breaks the all-you-can-eat commodity dynamic.

BUSINESS IMPACT

- Premium pricing for guaranteed SLAs vs. best-effort creates new margin pool

- Enterprise adoption of private 5G use cases that require performance guarantees

- Creates natural packaging with private networks, edge compute, and managed IoT

- Gartner: QoD and slicing are among the primary enterprise monetization levers for 5G investment recovery

WHAT LEADERS MUST DO

- Accelerate 5G Standalone deployment — slicing requires SA architecture

- Package performance tiers commercially with clear enterprise value propositions

- Develop slicing management tools that allow enterprise customers to self-serve provisioning

Trend #13 — Network Digital Twins: The Operational Backbone

THE SHIFT

From physical network management based on historical data and human expertise toward real-time virtual representations of the network enabling simulation, scenario modeling, energy optimization, and AI training before any change touches production.

WHY THIS EXISTS

Autonomous network ambitions repeatedly fail when tested against real network complexity — digital twins provide the safe simulation layer that makes autonomous decisioning trustworthy. Accenture, IDC, Nokia (AVA platform), and Ericsson all identify digital twins as a priority 2025–2026 investment. Energy optimization requires granular, real-time visibility across network elements — impossible without a digital twin layer.

BUSINESS IMPACT

- Directly reduces truck rolls by simulating configuration changes before deployment

- Cuts mean-time-to-repair through scenario-based diagnosis

- Enables zero-touch provisioning validated in simulation before live execution

- Enables synthetic data generation for AI training that preserves operational realism without risking production

- Prerequisite for closed-loop remediation — closed-loop systems cannot safely test remediation actions without a twin

WHAT LEADERS MUST DO

- Build network digital twin capability as foundational infrastructure investment — not an innovation lab project

- Integrate twin with live telemetry, OSS/BSS, and field data for continuous synchronization

- Use the twin for energy optimization immediately — the ROI case is faster and more defensible than autonomous assurance

Meta-Force 3: Revenue Expansion Beyond Commodity Connectivity

Trend Deep-Dives

Trend #14 — Private 5G and Private Wireless as Enterprise Platforms

THE SHIFT

From selling 5G as a consumer connectivity upgrade toward deploying private 5G as enterprise operational infrastructure — dedicated networks running manufacturing floors, hospital campuses, logistics hubs, and smart city infrastructure.

WHY THIS EXISTS

The global private networks market is projected to expand from $1.2B in 2024 to $21B by 2030 (Dell’Oro/Accenture). AT&T, T-Mobile, and Vodafone are actively deploying private 5G with hyperscalers for industrial use cases including predictive maintenance and worker safety (IDC/IFS, 2026).

BUSINESS IMPACT

- Premium enterprise contracts with multi-year durations vs. monthly consumer churn

- Natural bundling with edge compute, IoT management, and AI analytics

- ARPU significantly higher than consumer equivalent

- Entry point for broader enterprise managed services relationships

WHAT LEADERS MUST DO

- Develop vertical-specific private 5G propositions — manufacturing, healthcare, logistics, and energy are the highest-conviction verticals

- Partner with hyperscalers and system integrators for enterprise deployment capability

- Build commercial and technical team capability to sell to OT buyers, not just IT buyers

Trend #15 — Industry-Specific Vertical Solutions

THE SHIFT

From selling bandwidth and SLAs to enterprise buyers toward delivering industry-specific outcomes — solutions built around the operational workflows, compliance requirements, and data environments of specific verticals.

WHY THIS EXISTS

McKinsey’s B2B survey of 3,000 decision-makers (2026) validates enterprise willingness to pay for telco value beyond connectivity. The research consensus across McKinsey, Accenture, and WEF: generic B2B connectivity is commoditizing at the same rate as consumer — vertical differentiation is the only sustainable margin.

BUSINESS IMPACT

- Higher deal values and longer contract durations than generic connectivity

- Reduced price sensitivity when the solution is embedded in operational workflows

- Natural expansion into managed services, data analytics, and AI as the relationship deepens

- Manufacturing, healthcare, automotive, logistics, and energy are primary addressable verticals in the near term

WHAT LEADERS MUST DO

- Select 2–3 verticals where the operator’s existing customer relationships, geographic presence, and network capabilities create genuine advantage

- Build vertical-specific sales, pre-sales, and delivery capability — do not sell vertical solutions with generic connectivity teams

- Co-develop use cases with anchor enterprise customers before scaling commercially

Trend #16 — Security, Identity, Fraud, and Trust Services as Products

THE SHIFT

From treating security and identity as cost centers toward packaging them as revenue-generating products sold to enterprise, government, and financial services buyers.

WHY THIS EXISTS

The telecom cybersecurity market is projected to reach $83.79B by 2029 at 16.9% CAGR. Gartner confirms CSPs are investing in comprehensive AI security and governance solutions as both a defensive requirement and an offensive revenue line. Telcos have real-time visibility into SIM usage, device behavior, and network anomalies that creates uniquely valuable fraud intelligence.

BUSINESS IMPACT

- New high-margin revenue lines from existing network capabilities

- Identity and SIM-based authentication is a natural extension of core telco assets

- Financial services, healthcare, and government will pay premium for regulated, auditable identity infrastructure

- Positions telco as a trust anchor in the AI economy — where AI agent authentication will require verified identity

WHAT LEADERS MUST DO

- Audit existing security and identity capabilities for commercial packaging potential

- Develop SIM-swap fraud prevention, device authentication, and network-based identity as named commercial products

- Engage government and financial services buyers directly — they are the highest-value customers for trust services

Trend #17 — AI-Enabled Managed Services Rebuilt for the Cloud-Native Era

THE SHIFT

From legacy managed services based on headcount and SLA monitoring toward AI-native managed services delivering automated operations, predictive intelligence, and continuous optimization with outcomes-based pricing.

WHY THIS EXISTS

Enterprise customers migrating to cloud need managed connectivity, security, and AI operations that traditional telco managed services cannot deliver. AI reduces delivery cost significantly — making managed services economically viable at smaller deal sizes. Accenture’s HFS ranking identifies managed services rebuilt around AI, cloud, and security as a primary telco growth lever.

BUSINESS IMPACT

- Higher margin than traditional managed services due to AI-driven delivery efficiency

- Stickier customer relationships — managed services embed telco into customer operations

- Expansion pathway into adjacent AI services, analytics, and cloud management

- Natural packaging with private 5G, edge compute, and security products

WHAT LEADERS MUST DO

- Redesign managed services delivery around AI-native operations, not headcount augmentation

- Develop outcomes-based pricing models that align telco incentives with customer results

- Invest in the orchestration platforms that allow AI-driven managed services to scale without proportional headcount growth

Trend #18 — Ecosystem and Partnership-Led B2B Growth (B2B2X)

THE SHIFT

From direct B2B sales toward platform-based ecosystem models where telcos enable third parties — developers, ISVs, hyperscalers, vertical integrators — to build and sell solutions on top of telco network capabilities.

WHY THIS EXISTS

IDC: over 25% of telecom revenue growth will come from API-based ecosystem plays by 2027. The hyperscaler model — build platforms, enable ecosystems, capture a share of everything built on top — is being adapted by the most forward-thinking operators. GSMA Open Gateway is the industry infrastructure for cross-operator ecosystem monetization.

BUSINESS IMPACT

- Revenue at scale without proportional sales and delivery headcount growth

- Developer ecosystems create compounding network effects

- Third-party applications drive incremental network usage

- Reduces the operator’s need to build every vertical solution internally

WHAT LEADERS MUST DO

- Build developer platform capability — documentation, sandboxes, SDKs, support, and commercial models

- Create a business development function focused on ecosystem partnership, not just direct enterprise sales

- Ensure API commercial models create genuine partner incentive — not just access

Trend #19 — Hyperpersonalized Customer Growth Using Behavioral AI

THE SHIFT

From segment-based marketing and generic service bundles toward AI-driven, individual-level personalization that anticipates customer needs, reduces churn, and increases ARPU through relevance rather than promotion.

WHY THIS EXISTS

Deloitte: intelligent offer management combined with behavioral analytics can improve conversion rates by 20% while simultaneously lowering churn. GenAI enables truly individualized service bundles — ARPU uplift of 5–10% is the modeled impact (Gartner/Deloitte). Real-time data architecture is the enabling prerequisite.

BUSINESS IMPACT

- 5–10% ARPU improvement through personalized offer management (Gartner/Deloitte)

- 20% improvement in conversion rates from AI-driven targeting

- Churn reduction through proactive intervention based on behavioral prediction

- Lower cost-per-acquisition through precision targeting vs. mass-market spend

WHAT LEADERS MUST DO

- Build the behavioral analytics foundation — customer data platform, real-time event streams, propensity models

- Move from campaign-based marketing to always-on AI-driven engagement

- Ensure consent and privacy architecture supports personalization — regulatory non-compliance destroys the value

Trend #20 — Fixed Wireless Access: The 5G Monetization Bridge

THE SHIFT

From treating FWA as a niche rural solution toward recognizing it as a mainstream 5G monetization vehicle — extracting revenue from mid-band spectrum already deployed, at minimal incremental cost.

WHY THIS EXISTS

PwC Global Telecom Outlook: North America is approaching a cable-to-fiber tipping point, with cable projected to lose first place during 2026. T-Mobile projecting 7–8 million FWA subscribers as a core revenue line. For operators with mid-band 5G spectrum already deployed, FWA extracts incremental revenue from sunk capex with minimal additional investment.

BUSINESS IMPACT

- Near-term revenue extraction from already-deployed 5G infrastructure

- Competitive threat to cable operators defending fixed broadband share

- Rural market expansion — new subscribers previously inaccessible via fixed infrastructure

- Enterprise campus use cases with premium pricing potential

WHAT LEADERS MUST DO

- Quantify FWA revenue opportunity against existing spectrum and coverage footprint — most operators underestimate this

- Develop dedicated FWA customer propositions — consumer home, enterprise campus, and rural community are distinct segments

- Monitor the cable response: incumbent cable operators will defend fixed broadband aggressively

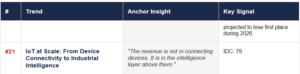

Trend #21 — IoT at Scale: From Device Connectivity to Industrial Intelligence

THE SHIFT

From selling SIM cards and connectivity to IoT devices toward building and operating the intelligence layer — real-time data pipelines, edge processing, vertical analytics, and managed IoT platforms — that makes connected devices genuinely valuable.

WHY THIS EXISTS

IDC: 79.4 zettabytes of data generated by connected IoT devices in 2025 alone. Cellular IoT connections projected to exceed 6.2 billion by 2030 — a $650B global market. 5G RedCap (Reduced Capability) makes cellular IoT economically viable for mass-scale sensor deployments. eSIM proliferation enables multi-network IoT and eliminates physical SIM logistics at scale.

BUSINESS IMPACT

- IoT connectivity alone is commoditizing — the margin is in the intelligence platform above it

- Managed IoT platforms for specific verticals command significantly higher contract values

- Real-time IoT data creates the raw material for AI analytics products and digital twin services

- Operators with IoT platform capability are more embedded in enterprise operations — higher switching costs

WHAT LEADERS MUST DO

- Build or acquire IoT platform capability — not just connectivity management

- Focus on 2–3 verticals where IoT creates genuine operational value: smart manufacturing, connected logistics, precision agriculture

- Develop IoT analytics products that turn device data into operational intelligence customers will pay for

Meta-Force 4: Telco in the AI Value Chain

Trend Summary

Trend Deep-Dives

Trend #22 — Telco as AI Backbone: Fiber, Sites, Transport, and Edge Locality

THE SHIFT

From viewing fiber and tower infrastructure as cost assets supporting consumer connectivity toward actively monetizing them as the foundational physical layer of the AI economy.

WHY THIS EXISTS

McKinsey: 55% of telco leaders identify AI infrastructure as a top strategic bet, citing potential ROIC improvement of up to 50%. Grid power constraints in major data center hubs are driving new subsea, long-haul, and metro fiber builds toward Tier-2 cities. Government national AI strategies are creating public funding and regulatory tailwinds for telcos with existing infrastructure.

BUSINESS IMPACT

- Potential ROIC improvement of up to 50% from AI infrastructure monetization (McKinsey, Jan 2026)

- New revenue from existing assets — fiber routes, tower sites, and power connections — with relatively low incremental investment

- Strategic positioning as national AI infrastructure — creating regulatory goodwill and public funding access

- AI-related data center infrastructure expected to generate more than $1 trillion in spending over next 5 years (Dell’Oro/Accenture)

WHAT LEADERS MUST DO

- Audit the AI infrastructure opportunity against existing fiber, tower, and power assets

- Develop the commercial and technical capability to serve hyperscaler and enterprise AI customers

- Engage government stakeholders actively — national AI strategies create funding and partnership opportunities for credible infrastructure providers

Trend #23 — Selective AI Infrastructure Monetization

THE SHIFT

From passive infrastructure ownership toward active monetization of the physical adjacencies AI infrastructure requires — power, cooling, connectivity, and geographic distribution that co-location and hyperscaler operators are competing fiercely to secure.

WHY THIS EXISTS

Massive AI infrastructure investment is reshaping telecom economics globally. AI-related data center infrastructure expected to generate more than $1 trillion over the next 5 years. Grid power constraints are driving demand for distributed, edge-located compute — exactly where telcos’ distributed tower and exchange infrastructure sits. Deutsche Telekom’s $1B NVIDIA initiative (10,000 Blackwell chips) is the operator archetype.

BUSINESS IMPACT

- New high-return revenue streams from existing physical assets with long-term anchor contracts

- Positions telco as a critical national AI infrastructure provider

- Long-term anchor contracts with hyperscalers and enterprise AI operators

- McKinsey: telcos exploring this space are seeing potential ROIC improvements of up to 50%

WHAT LEADERS MUST DO

- Identify sites with the best combination of power access, fiber connectivity, and proximity to AI demand centers

- Develop the commercial model — colocation, wholesale power, connectivity, and managed compute are different products requiring different go-to-market approaches

- Be selective: not every operator has the asset quality and capital base to compete in hyperscale AI infrastructure

Trend #24 — Sovereign AI: Telco as the National Compute Layer

THE SHIFT

From positioning as a generic cloud and connectivity provider toward active participation in national sovereign AI infrastructure — building and operating AI compute within jurisdictional boundaries as required by government mandate.

WHY THIS EXISTS

IDC (March 2026): sovereign AI crystallizes around inferencing in 2026 — telcos have genuine structural advantage due to local infrastructure, regulatory relationships, and national trust. Sovereign AI and sovereign cloud global spending projected to reach $258.5B by 2027 — three times the 2022 level (IDC, cited by Accenture). Deutsche Telekom’s sovereign Germany stack (NVIDIA + SAP + T-Systems) is the most advanced operator implementation.

BUSINESS IMPACT

- Access to government funding and procurement for credible sovereign infrastructure providers

- Long-term contracts with regulated enterprises — financial services, healthcare, defense — that cannot use non-sovereign alternatives

- Competitive differentiation that hyperscalers structurally cannot match in markets with strict data residency requirements

- Vodafone (Jan 2026): ‘The relevance of sovereign AI will be paramount in 2026’

WHAT LEADERS MUST DO

- Map sovereign AI requirements in each operating market — legislation, mandates, and funding programs differ significantly by country

- Build the partnership stack: national sovereign AI requires infrastructure (telco), compute (GPU vendors), platform (cloud software), and compliance partners

- Position the telco’s regulated status, local presence, and national trust as commercial assets — not compliance burdens

Trend #25 — Metro Edge and Inference Adjacency for Low-Latency AI

THE SHIFT

From centralized cloud inference toward distributed edge inference deployed at or near network edge nodes — enabling sub-10ms latency for AI applications that centralized data centers cannot physically deliver.

WHY THIS EXISTS

Gartner: by 2027, 40% of AI inference tasks will occur at the network edge. IDC (March 2026): AI adoption is crystallizing around inferencing — and telcos have a genuine structural advantage due to their distributed infrastructure. Autonomous vehicles, industrial robotics, AR/VR, and real-time AI agents all require inference latency that only edge deployment can deliver.

BUSINESS IMPACT

- New revenue from edge compute hosting — differentiated by latency guarantees centralized cloud cannot match

- Premium pricing for guaranteed sub-millisecond inference adjacency in manufacturing, automotive, and healthcare

- Positions existing tower and exchange infrastructure as a strategic AI asset rather than a legacy cost base

WHAT LEADERS MUST DO

- Develop the edge compute product — hardware, connectivity, management, and SLA — as a commercial offering, not a technology demonstration

- Target latency-sensitive verticals first: autonomous vehicles, industrial automation, AR/VR, and real-time AI analytics

- Build partnerships with AI software vendors that will deploy on telco edge infrastructure

Trend #26 — Telco as Trusted AI Distribution and Marketplace Layer

THE SHIFT

From passive connectivity provider toward active role as trusted AI distribution layer — curating, distributing, and governing AI services to enterprise and consumer customers using identity, network control, and regulatory standing as competitive differentiators.

WHY THIS EXISTS

WEF’s 2026 paper frames this as an explicit pathway: telcos as trusted AI marketplace layers. AI agent authentication will require verified, regulated identity infrastructure that cloud providers cannot provide with the same legal standing as telcos in regulated markets. IDC: consumers will spend $100B via AI agents on smartphones by 2027 — telcos are positioned to be the trusted authentication and billing layer.

BUSINESS IMPACT

- Revenue share from AI services distributed through telco channels

- Identity and authentication services becoming AI-era infrastructure primitives

- Natural expansion from connectivity provider to AI services broker

- Billing relationships, consent infrastructure, and device management create natural commercial rails for AI service distribution

WHAT LEADERS MUST DO

- Develop the AI marketplace product — starting with enterprise AI service procurement through trusted telco channels

- Build the identity and authentication infrastructure that enables AI agent verification at network level

- Partner with AI vendors to create go-to-market through telco commercial channels

Trend #27 — NaaS: Network as a Service as the Software Product Layer

THE SHIFT

From selling network capacity as a fixed-price committed service toward cloud-like, consumption-priced, API-driven connectivity that enterprises provision, manage, and scale on demand.

WHY THIS EXISTS

Telefónica’s Dynamic Network NaaS offering is the most advanced operator implementation: real-time provisioning, multi-cloud connectivity, and automated management through API-based interfaces. Enterprise buyers accustomed to consumption-based cloud models are applying the same expectations to connectivity. NaaS creates a natural commercial bridge between connectivity and cloud services.

BUSINESS IMPACT

- Consumption-based pricing captures upside from traffic growth that flat-rate pricing misses

- API-driven self-service reduces commercial friction and accelerates enterprise adoption

- Natural bundling with edge compute, private 5G, and managed AI services

- Positions telco as a credible alternative or complement to hyperscaler networking products (AWS Direct Connect, Azure ExpressRoute)

WHAT LEADERS MUST DO

- Build NaaS as a product with genuine self-service capability — not a rebranded connectivity contract

- Develop the API layer and developer tooling that makes NaaS genuinely programmable

- Price for consumption — align commercial model with enterprise value delivered, not infrastructure cost incurred

Meta-Force 5: Trust, Resilience, and Sovereign Control

Trend Summary

Trend #28 — Operational Resilience as a Commercial Differentiator

THE SHIFT

From treating operational resilience as infrastructure reliability management toward positioning it as a commercially differentiated capability with contractual SLAs, transparent performance reporting, and premium pricing for critical enterprise customers.

WHY THIS EXISTS

WEF warns that cyberattacks on telecom can have a domino effect on entire economies. Gartner: 70% of telecom operators will adopt AI-based cybersecurity to prevent outages and data breaches by 2026. Regulatory requirements (EU NIS2, DORA) are making resilience a procurement criterion rather than an assumption.

BUSINESS IMPACT

- Premium pricing for resilience-guaranteed services to critical infrastructure customers

- Regulatory compliance as a commercial asset — regulated enterprise buyers require provably resilient connectivity

- Resilience SLAs create differentiation that commodity connectivity providers cannot match

WHAT LEADERS MUST DO

- Develop resilience as a commercial product with transparent SLAs, monitoring dashboards, and contractual commitments

- Invest in AI-driven proactive resilience — predicting and preventing failures before they impact customers

- Report resilience performance publicly — transparency builds trust with enterprise buyers

Trend #29 — Cybersecurity Embedded Into Networks, Products, and Operations

THE SHIFT

From perimeter-based security added as a layer on top of network infrastructure toward security embedded natively into every network function, API, AI agent, and enterprise service — with AI-driven threat detection and response operating in real time.

WHY THIS EXISTS

The telecom cybersecurity market is projected to reach $83.79B by 2029 at 16.9% CAGR. Open RAN, network API exposure, and agentic AI deployment are dramatically expanding the attack surface — each new interface is a potential entry point. State-sponsored attackers are specifically targeting telco infrastructure as national security-critical assets.

BUSINESS IMPACT

- Security as an embedded differentiator for enterprise customers vs. commodity connectivity

- Managed security services as a high-margin product line

- Regulatory non-compliance costs exceed security investment — the ROI case is straightforward

- AI-driven threat detection enables real-time response that legacy security tooling cannot achieve

WHAT LEADERS MUST DO

- Implement zero-trust architecture across network and enterprise services

- Develop AI-driven threat detection and response as both an operational capability and a commercial product

- Address API security specifically — every network API exposure creates a potential attack vector that must be governed

Trend #30 — Digital Sovereignty and Jurisdictional Control of Data and AI

THE SHIFT

From treating data residency as a compliance checkbox toward building genuine sovereign data and AI infrastructure where data stays within jurisdictional boundaries and enterprises have verifiable control.

WHY THIS EXISTS

Vodafone’s 2026 predictions: ‘In 2026, data sovereignty will take centre stage — sovereign clouds give companies control over their data, protect privacy, and adapt to geopolitical shifts.’ Gartner’s geopatriation trend: relocation of workloads from global hyperscalers to regional or national alternatives — going beyond data sovereignty to operational and technical sovereignty. EU AI Act, GDPR enforcement, and sector-specific regulations are making sovereign infrastructure a procurement requirement.

BUSINESS IMPACT

- Access to regulated markets (financial services, healthcare, defense) requiring sovereign infrastructure

- Competitive advantage over hyperscalers in markets with strict data residency requirements

- Government partnerships and public funding for national sovereign AI infrastructure

- Accenture: sovereign data and cloud global spending projected to reach $258.5B by 2027 — three times the 2022 level

WHAT LEADERS MUST DO

- Develop sovereign infrastructure products that give enterprise customers verifiable jurisdictional control

- Partner with national AI strategy programs — governments are actively funding sovereign AI and need credible infrastructure partners

- Distinguish genuine sovereignty (technical and operational) from marketing sovereignty — enterprise and government buyers are sophisticated

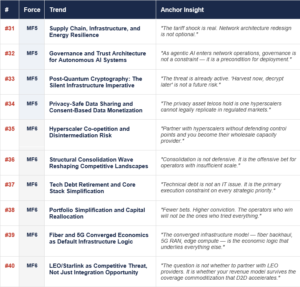

Trend #31 — Supply Chain, Infrastructure, and Energy Resilience

THE SHIFT

From assuming stable, globally optimized supply chains toward building resilient, regionally diversified procurement and infrastructure strategies that can absorb geopolitical disruption, equipment bans, and tariff shocks.

WHY THIS EXISTS

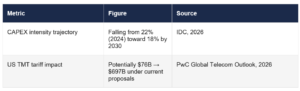

PwC: annual US tariff measures affecting TMT supply chains could rise from ~$76B to nearly $697B under current proposals — raising hardware costs and complicating capital planning. Equipment bans (Huawei, ZTE) in multiple markets are forcing wholesale RAN replacement. Grid power constraints and energy price volatility are creating infrastructure resilience requirements beyond traditional redundancy.

BUSINESS IMPACT

- Operators with diversified supply chains maintain capex predictability; those without face significant budget overruns

- Energy resilience (backup power, renewable sourcing, on-site generation) reduces cost volatility and regulatory risk

- Supply chain resilience becomes a contractual requirement for government and defense customers

WHAT LEADERS MUST DO

- Diversify RAN and network hardware vendors — Open RAN is the architectural enabler

- Build energy resilience into all new infrastructure deployments — renewable power, battery backup, and on-site generation

- Create procurement resilience through multi-vendor frameworks and regional sourcing alternatives

Trend #32 — Governance and Trust Architecture for Autonomous AI Systems

THE SHIFT

From ad-hoc AI governance policies toward systematic trust architecture — explicit policies, decision rights, audit trails, and accountability frameworks governing every AI agent and autonomous system operating in the network and customer domains.

WHY THIS EXISTS

Gartner’s top I&O trend for 2026: AI governance platforms that incorporate responsible AI practices, manage bias, protect data, validate models, and address compliance risks. Agentic AI systems operating in network management and customer care make consequential autonomous decisions — governance determines whether these can be safely deployed at scale. EU AI Act and sector-specific rules are making AI governance a compliance requirement.

BUSINESS IMPACT

- Governance as a prerequisite for deploying agentic AI in critical network and customer operations

- Trust architecture creates competitive differentiation with enterprise customers who require auditable AI decisions

- Governance failures in AI deployment create regulatory, reputational, and operational risk that can offset AI’s productivity gains

WHAT LEADERS MUST DO

- Implement AI governance frameworks before scaling agentic systems — not after incidents occur

- Define explicit policies for AI agent decision authorities — what decisions agents can make autonomously vs. with human oversight

- Create audit trails for all consequential AI decisions in network operations and customer management

Trend #33 — Post-Quantum Cryptography: The Silent Infrastructure Imperative

THE SHIFT

From treating quantum-safe cryptography as a 2030 planning item toward treating it as an active procurement and architecture decision that must begin now.

WHY THIS EXISTS

NIST finalized its first post-quantum cryptography standards in August 2024: CRYSTALS-Kyber for key encapsulation, CRYSTALS-Dilithium for digital signatures. ‘Harvest now, decrypt later’ attacks are already documented — adversaries capturing encrypted telco traffic today for decryption when quantum computers reach sufficient capability (estimated 2030–2035 by intelligence assessments). WEF’s 2025 Quantum Technologies report specifically identifies telecommunications as a priority sector for quantum-safe network transitions.

BUSINESS IMPACT

- Operators beginning crypto-agility architecture today have a multi-year head start on those treating this as a 2029 problem

- Quantum-safe infrastructure is becoming a requirement for government and defense contracts — procurement conversations are already active

- Migration complexity (encryption in every stack layer) means the cost of late action is significantly higher than early action

WHAT LEADERS MUST DO

- Begin cryptographic inventory now — map every system, interface, and protocol that relies on encryption

- Adopt crypto-agility architecture — design systems to swap cryptographic algorithms without full stack replacement

- Engage with NIST PQC standards and begin pilot implementation in the highest-risk systems first (authentication, identity, financial transactions)

Trend #34 — Privacy-Safe Data Sharing and Consent-Based Data Monetization

THE SHIFT

From treating privacy as a compliance cost toward building privacy-safe data products — using consent infrastructure, anonymization, and privacy-preserving compute to create monetizable data assets while maintaining regulatory compliance.

WHY THIS EXISTS

Privacy-preserving technologies (differential privacy, federated learning, secure multiparty computation) now enable data monetization without exposing individual records. Enterprise and government buyers require provably compliant data — telcos with auditable consent infrastructure have a commercial advantage over digital platforms operating in legal grey areas.

BUSINESS IMPACT

- Consent-based data products for advertising, insurance, financial services, and government that command premium pricing

- Privacy-preserving analytics as a service — telco as a trusted data broker for industries that need behavioral intelligence without PII exposure

- Regulatory compliance as a commercial differentiator vs. digital platforms operating in legal grey areas

WHAT LEADERS MUST DO

- Build consent infrastructure that is genuine and auditable — not checkbox compliance

- Invest in privacy-preserving technology that enables data utility without PII exposure

- Develop the commercial models for data products — pricing, partner agreements, regulatory frameworks

Meta-Force 6: Capital Choices, Competitive Power Shifts & Strategic Optionality

Trend Summary

Trend Deep-Dives

Trend #35 — Hyperscaler Co-opetition and Disintermediation Risk

THE SHIFT

From viewing hyperscalers primarily as vendors and customers toward managing them as structural co-opetitors simultaneously moving up the stack (into managed connectivity) and down the stack (into edge compute and telecom cloud).

WHY THIS EXISTS

Deutsche Telekom’s dual strategy — Google partnership plus sovereign cloud build — is the most sophisticated operator response to this tension. Vodafone’s deep Microsoft alliance provides cloud scale but reduces sovereign independence. Google Distributed Cloud, Azure for Operators, and AWS Wavelength are all active telco encroachment programs.

BUSINESS IMPACT

- Operators without an explicit hyperscaler strategy will find their differentiated control points captured over a 3–5 year horizon

- Partnership without defense creates dependency — reducing negotiating power and margin over time

- Telcos that defend identity, regulated trust, local presence, and network intelligence create structural advantages hyperscalers cannot replicate

WHAT LEADERS MUST DO

- Define explicit hyperscaler strategy: where to partner, where to compete, and where to defend

- Map the control points that must remain telco-owned: identity, network intelligence, regulatory standing, local presence

- Adopt Deutsche Telekom’s dual-strategy model as the reference: partner where scale matters, build where sovereignty matters

Trend #36 — Structural Consolidation Wave Reshaping Competitive Landscapes

THE SHIFT

From organic growth and incremental portfolio optimization toward strategic M&A as the primary lever for achieving the scale, synergies, and portfolio differentiation required to fund AI transformation while maintaining competitive returns.

WHY THIS EXISTS

McKinsey (Jan 2026, n=125): close to 60% of telco leaders identify M&A as a top priority. Charter Communications’ $34.5B acquisition of Cox Communications (May 2025), Vodafone UK + Three UK creating the UK’s largest mobile operator, Orange Spain + MasMovil. European regulators have approved key in-market mergers with network investment commitments — signaling broader regulatory acceptance. Synergies of 15%+ of combined capex and 30%+ of combined opex are the modeled outcomes (McKinsey).

BUSINESS IMPACT

- Scale creates the capital base for AI transformation that subscale operators cannot fund independently

- In-country consolidation reduces competitive intensity and improves pricing power

- Portfolio optimization through divestitures frees capital for higher-return bets

- 80% of media industry leaders surveyed expect M&A to increase significantly in 2026 and beyond (McKinsey)

WHAT LEADERS MUST DO

- Develop a clear M&A thesis aligned with strategic positioning: which assets create scale, which create capability, which should be divested

- Engage regulatory stakeholders proactively — regulators are approving more consolidation but with investment conditions attached

- Manage integration risk: most telecom M&A value destruction happens in integration, not deal execution

Trend #37 — Tech Debt Retirement and Core Stack Simplification

THE SHIFT

From managing technical debt as a known but deprioritized IT cost toward treating it as a strategic risk that blocks AI adoption, autonomous networks, real-time systems, and the operating model redesign that every other trend on this list requires.

WHY THIS EXISTS

IDC (2026): 52% of telco C-suite leaders have AI implementation as a top-3 priority; 50% simultaneously have IT modernization as a top-3 priority — these compete for the same constrained capital pool. McKinsey: scaling AI requires cross-functional teams and rapid test-and-learn cycles — impossible on fragmented, brittle legacy architectures.

BUSINESS IMPACT

- Technical debt is the hidden cost multiplier behind every transformation program — making everything slower and more expensive

- Operators who retire technical debt create a structural execution advantage over those who layer new capability on legacy foundations

- Simplification frees engineering capacity from maintenance to innovation

WHAT LEADERS MUST DO

- Make technical debt retirement an executive priority with C-suite ownership, not an IT program

- Create a technical debt register with business impact quantification — translate legacy complexity into revenue and cost terms

- Sequence simplification around the capabilities that unlock the highest-value transformation programs first

Trend #38 — Portfolio Simplification and Capital Reallocation

THE SHIFT

From attempting to maintain broad portfolios across consumer, enterprise, wholesale, media, fintech, and technology toward deliberate portfolio pruning — concentrating capital on 3–4 differentiated bets with clear time-to-value.

WHY THIS EXISTS

PwC’s TelcOS thesis explicitly advocates ‘puretone’ portfolio models: fewer, cleaner, higher-conviction bets. Telecom CAPEX intensity declining toward 18% by end of decade (IDC) — operators cannot fund every adjacency. WEF explicitly warns against telcos trying to be connectivity leader, AI techco, and sovereign champion simultaneously without the capital base.

BUSINESS IMPACT

- Concentrated capital produces higher returns than distributed capital across too many priorities

- Simplified portfolios reduce operational complexity and improve execution velocity

- Divestitures of non-core assets generate capital for transformation investment

WHAT LEADERS MUST DO

- Conduct rigorous portfolio review: apply return, differentiation, and strategic fit criteria to every business line

- Commit to public portfolio simplification as a strategic signal — investors and customers respond to clarity

- Reallocate capital more aggressively than the board is comfortable with — incremental reallocation produces incremental outcomes

Trend #39 — Fiber and 5G Converged Economics as Default Infrastructure Logic

THE SHIFT

From treating fiber and 5G as parallel investment programs toward an integrated converged infrastructure model where fiber provides backhaul, 5G provides access, and edge compute sits at the intersection — supporting consumer, enterprise, and AI workloads from a single asset base.

WHY THIS EXISTS

McKinsey: fiber deal multiples declining (20x EBITDA in 2022 to ~19x in 2025); tower multiples falling faster (22x to 17x). AI and data center investment is reshaping fiber demand — new subsea, long-haul, and metro fiber builds toward secondary markets driven by compute demand. FWA extraction from mid-band 5G infrastructure makes the converged model more capital-efficient than separate fiber and wireless programs.

BUSINESS IMPACT

- Converged infrastructure reduces per-unit capex vs. separate fiber and wireless programs

- Single asset base serves consumer broadband, enterprise connectivity, and AI infrastructure simultaneously

- LEO satellite integration completes the converged model — providing backhaul and access in geographies where terrestrial infrastructure economics do not work

WHAT LEADERS MUST DO

- Develop an integrated converged infrastructure investment strategy — not separate fiber and 5G capex programs

- Evaluate tower and fiber portfolio monetization: infrastructure funds are active buyers of telecom passive infrastructure

- Build the edge compute layer into fiber and 5G deployment programs from the start — retrofitting is significantly more expensive

Trend #40 — LEO/Starlink as Competitive Threat, Not Just Integration Opportunity

THE SHIFT

From treating LEO satellites as a complementary technology and partnership opportunity toward acknowledging the direct competitive threat — particularly from direct-to-device (D2D) capability moving toward replacing mobile coverage in areas where MNOs have historically held monopoly.

WHY THIS EXISTS

McKinsey estimates LEO could capture close to 20% of fiber’s existing addressable market. Starlink’s satellite-to-smartphone capability, T-Mobile’s partnership with SpaceX, and AST SpaceMobile’s broadband constellation are moving toward replacing mobile coverage in rural areas. IDC: by 2027, consumers will spend $100B via AI agents running independently on smartphones — requiring ubiquitous connectivity that satellite D2D can deliver regardless of tower coverage.

BUSINESS IMPACT

- Rural and developing market operators face direct revenue displacement as D2D coverage eliminates the coverage advantage justifying rural mobile pricing

- Coverage commoditization in areas where MNOs currently hold pricing power

- Wholesale market disruption — LEO creates alternative backhaul routes reducing telco wholesale pricing power

- Upside: telcos that partner early can use satellite to reduce rural capex and serve previously uneconomic geographies

WHAT LEADERS MUST DO

- Model the LEO disruption scenario explicitly — quantify the revenue at risk from D2D coverage commoditization in each operating market

- Develop a LEO partnership strategy as a defensive move: use satellite to reduce rural infrastructure capex rather than wait to be disrupted

- Monitor AST SpaceMobile, Starlink, and OneWeb D2D deployment timelines — the competitive threat timeline is 3–5 years, not 10

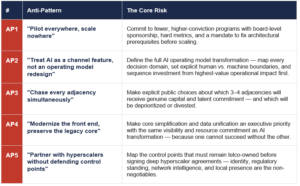

5 Anti-Patterns: What Consistently Fails

These are the patterns that look attractive but repeatedly destroy value. Each is sourced from operator case evidence and research consensus — not analytical inference.

AP1 — “Pilot everywhere, scale nowhere”

WHAT IT LOOKS LIKE

Dozens of AI, API, and digital pilots running simultaneously across business units, each with a compelling demo — none producing measurable EBITDA impact.

THE EVIDENCE

McKinsey: AI driving less than 2% of total revenues for more than half of operators that have tested AI use cases, despite years of piloting. The cause is consistent: no data foundation fix, no operating model change, no cross-functional ownership of outcomes.

THE COUNTER-MOVE

Commit to fewer, higher-conviction programs with board-level sponsorship, hard metrics, and a mandate to fix architectural prerequisites before scaling.

AP2 — “Treat AI as a channel feature, not an operating model redesign”

WHAT IT LOOKS LIKE

AI investment concentrated in customer-facing chatbots and recommendation engines while network operations, engineering, field service, and financial operations remain unchanged.

THE EVIDENCE

The research consensus across McKinsey, Accenture, WEF, and IDC: the structural cost and revenue value of AI is in network assurance, engineering automation, field service, knowledge work, and financial decisioning — not the front-end.

THE COUNTER-MOVE

Define the full AI operating model transformation — map every decision domain, set explicit human vs. machine boundaries, and sequence investment from highest-value operational impact first.

AP3 — “Chase every adjacency simultaneously”

WHAT IT LOOKS LIKE

A strategic plan committing the operator to connectivity leadership, enterprise platform, AI techco, sovereign infrastructure, fintech, and media simultaneously — with insufficient capital, talent, or focus to execute any credibly.

THE EVIDENCE

WEF’s 2026 paper explicitly frames the choice: modern connectivity leader, AI techco, or national sovereign champion. PwC advocates ‘puretone’ portfolio models for exactly this reason. Accenture: operators that try to modernize networks, build digital cores, and capture every adjacency simultaneously overwhelm their change capacity.

THE COUNTER-MOVE

Make explicit public choices about which 3–4 adjacencies will receive genuine capital and talent commitment — and which will be deprioritized or divested.

AP4 — “Modernize the front end, preserve the legacy core”

WHAT IT LOOKS LIKE

Investment in digital customer experience and AI-powered care — all layered on top of fragmented OSS/BSS, brittle integration middleware, and 20-year-old network inventory systems.

THE EVIDENCE

IDC EMEA survey: interoperability failures and the lack of a single source of truth in network data are the top two barriers to both autonomous networks and AI value realization. Accenture’s reinvention blueprint is explicit: the digital core comes first.

THE COUNTER-MOVE

Make core simplification and data unification an executive priority with the same visibility and resource commitment as AI transformation — because one cannot succeed without the other.

AP5 — “Partner with hyperscalers without defending control points”

WHAT IT LOOKS LIKE

Deep partnership with one or two hyperscalers that provides cloud scale and AI tooling — but gradually transfers differentiated assets (identity, network intelligence, customer data) to the hyperscaler platform.

THE EVIDENCE

Deutsche Telekom explicitly identified this risk and responded with a dual strategy — Google partnership for specific capabilities plus its own sovereign cloud infrastructure. Vodafone’s deep Microsoft dependence is the contrasting model Deutsche Telekom is explicitly differentiating against.

THE COUNTER-MOVE

Map the control points that must remain telco-owned before signing deep hyperscaler agreements — identity, regulatory standing, network intelligence, and local presence are the non-negotiables.

7 CEO Priorities: Next 12–24 Months

Seven priorities that emerge from the research consensus. Each is sequenced by urgency and strategic leverage, not alphabetically.

P1 — Pick a role in the AI value chain and commit capital to it

Modern connectivity leader, AI-enabled B2B platform, or sovereign infrastructure champion. WEF, McKinsey, and IDC all converge on this imperative. The cost of trying all three is higher than the cost of a wrong choice — and the cost of no choice is highest of all.

P2 — Move AI from pilot portfolio to operating model redesign

Tie every AI program to hard metrics: opex per site, truck rolls, MTTR, churn rate, deal velocity, and margin protection. McKinsey: only 47% of telcos have seen measurable AI impact despite 61% scaling programs. The gap is operating model, not technology.

P3 — Treat tech debt and data fragmentation as strategic risks, not IT backlog

IDC is explicit: the same barriers blocking autonomous networks block AI value realization. Data governance, network inventory accuracy, and architectural debt are CEO-level issues disguised as IT issues.

P4 — Build 3–4 revenue pools beyond commodity connectivity with time-bound business cases

Typical high-conviction candidates: private wireless, security/identity/trust services, vertical B2B solutions, network APIs, AI-enabled managed services. Not all five — pick those your asset base, market position, and existing customer relationships support.

P5 — Rewire the operating model around platforms and products

Speed, reuse, and scaling all fail if the org structure remains project-based and siloed. McKinsey’s Rewired framework (2nd edition, April 2026): cross-functional teams, rapid test-and-learn cycles, and continuous improvement embedded into daily execution are the organizational prerequisites.

P6 — Define your hyperscaler strategy explicitly and enforce it

Partner where cloud scale, AI tooling, and distribution matter. Defend where local trust, regulatory standing, network intelligence, and sovereign compute requirements create moats that hyperscalers cannot legally or structurally replicate.

P7 — Reallocate capital more aggressively than the board is comfortable with

PwC: the strategic question is no longer whether telecoms will become AI-native — it is how fast leadership can progress from pilots to a new operating system. Incremental reallocation produces incremental outcomes.

7 Blockers: What Gets in the Way

The barriers that determine whether strategy becomes execution. Each blocker is cited across multiple independent research sources — they are structural, not circumstantial.

B1 — Legacy OSS/BSS and integration complexity

The hidden drag behind AI, APIs, real-time systems, and faster product launch. Identified as the primary structural barrier by IDC, Gartner, Accenture, and TM Forum. Every AI program that fails on data quality traces back to this root cause.

B2 — Fragmented data and no single operational truth

IDC EMEA survey (July 2025, n=150): interoperability failures and the persistent lack of a single source of truth in network data are the top two constraints on both autonomous networks and AI adoption. These are the same problem in two symptoms.

B3 — Capital scarcity competing with too many investment priorities

CAPEX intensity declining toward 18% by end of decade (IDC). 52% of C-suite leaders have AI as a top-3 priority; 50% simultaneously have IT modernization as a top-3 priority. These compete for the same constrained capital.

B4 — AI, cloud, and software talent scarcity

Accenture: 76% of CSP executives need to upskill employees in GenAI within 3 years. The competitive market for AI engineers and cloud-native developers places telcos in direct competition with hyperscalers at a structural pay and culture disadvantage.

B5 — Organizational silos and slow execution culture

Transformation stalls not because strategy is wrong, but because ownership, incentives, and platform governance are fragmented across legacy organizational lines. McKinsey’s Rewired framework (April 2026) identifies organizational model as the decisive execution variable.

B6 — Regulatory asymmetry and sovereignty complexity

Telcos face heavier regulatory obligations than digital competitors while simultaneously being expected to provide trusted national AI infrastructure. Spectrum policy, data residency rules, equipment bans, and sector-specific AI regulations create compliance costs that consume capital intended for transformation.

B7 — Weak commercial packaging of differentiated assets

Most operators own assets that matter — regulated identity, network-level trust, local physical presence, real-time behavioral data — but still sell them as generic connectivity rather than outcome-based solutions. The packaging gap, not the asset gap, is the primary revenue problem.

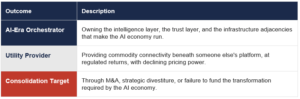

Closing Perspective: Five Choices That Decide Everything

Telecom is not competing on infrastructure anymore. It is competing for control of value flows.

The next 12–24 months will decide three things:

The Five Choices That Decide the Outcome

Forty trends are forcing functions. They do not decide the outcome. Leadership choices decide the outcome:

The window for these choices is narrowing. The operators who act in 2026 will define the industry’s winner map through 2030.

Sources: Gartner (I&O Trends 2026, Strategic Technology Trends 2026, CSP AI Security Report 2026) · McKinsey (CxO Survey January 2026 n=125, Telecom Value Creation February 2026, TMT M&A Report February 2026, MWC 2026 AI Briefing) · Accenture (Telecom Renaissance Report 2025, AI-Powered Trends 2025, HFS Telecom Horizons 2025) · IDC (Telco Forum Barcelona March 2026, EMEA Telco Transformation Survey July 2025 n=150, C-Suite Tech Survey September 2025 n=45) · World Economic Forum (Strategic Role of Telecom in AI Value Chain 2026, GenAI in Telecom 2025, Quantum Technologies Report 2025) · PwC (Global Telecom Outlook 2025–2029) · Vodafone (Fast Forward Predictions January 2026) · Deutsche Telekom (Sovereign Germany Stack Program 2025) · GSMA Intelligence · TM Forum (Autonomous Networks Benchmark 2025)

Leave a Reply