The state of technology services in 2026: The AI Services Revolution

AI is the reason why the services era is back.

“AI enabling outcomes” is a hot topic right now. That’s right. But here’s what most leaders don’t get: AI doesn’t get rid of services; it makes them necessary.

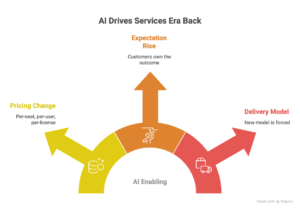

AI is at the same time:

- Changing the way things are priced (per-seat, per-user, per-license)

- raising customer expectations (you own the outcome, not the tool)

- forcing a new delivery model (because the “last mile” is hard in real businesses).

Incumbents have a lot of services, but many are cutting them because they think AI will do the work. Startups are doing the opposite: they’re spending billions to build the same things that established companies are tearing down. No one has a clean playbook yet. That’s the time we’re in.

1) AI economics isn’t the same as “GenAI in the product.” It’s a reset of the business model.

“SaaS physics” was what the cloud/SaaS era was based on:

- Customers paid for access (seats),

- Growth came from getting more users, and

- Services were a necessary evil to get people to use the product.

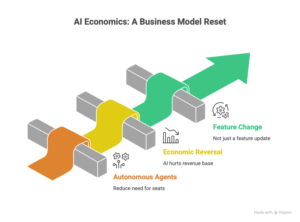

This model doesn’t work with autonomous agents.

Agents do the work, which means fewer people need seats. If your income depends on seats, then the better your AI works, the more you hurt your own base. That’s the main problem that people who are already in power are facing.

This isn’t a change in features. It’s an economic reversal.

2) The market is breaking up into three types of financial DNA.

TSIA’s framing is clear: T&S 50, Cloud 40, and AI 20.

T&S 50: the big, grown-up companies

Stable, profitable, and slow growth. Their first move is always to defend:

- “Let’s add AI”

- “Let’s keep the install base safe”

That’s not a plan; it’s putting things off.

Cloud 40: the best SaaS companies

High growth, low profitability, and cost structures that are heavy on sales and marketing. They have to deal with two problems:

Seat prices are at risk because their cost base is already stretched.

AI 20: the people who are trying to beat it

A lot of growth and a lot of losses, on purpose. They don’t sell tools. They’re selling results and putting a lot of money into delivery muscle. It’s not about whether they’re losing money. The point is that they’re putting in place the new infrastructure for shipping outcomes.

3) Product-led growth hits a wall: AI projects die in the “last mile.”

In the beginning, the story was “APIs + models + self-serve adoption.”

What really happens in businesses:

- old systems,

- messy data,

- security problems,

- governance problems,

- too many integrations.

This environment isn’t good for a raw model on its own. The gap between proof-of-concept and production is the most important one, and that gap is mostly services.

That means the old world of “ship it and forget it” is over. The new world is

Be responsible for the result, or someone else will.

If you don’t offer the integration, operations, tuning, and governance layer, the customer will find it somewhere else, like from AI-native MSPs, SIs, or small businesses, and you’ll lose the relationship. One risk that leaders always underestimate is that AI programs often turn into a lot of the same hard work, like cleaning up data, integrating it, managing it, and keeping it safe. If this isn’t planned and packaged carefully, high-margin software and outcomes quickly turn into low-margin “data plumbing.” Serious players see data readiness and integration as a productized service line, not as a hidden cost.

The Five Trends That Will Shape Technology Services

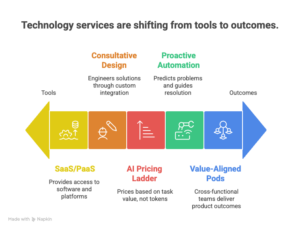

Trend 1: Offers change from SaaS/PaaS to Outcome-as-a-Service

The offer is no longer just “here’s a tool.” It turns into:

- “We’ll handle 50% of tickets on our own,”

- “We’ll cut down on fraud by X,” and

- “We’ll improve inventory by Y.”

This changes the risk model:

- In the past, customers were responsible for ROI risk.

- Vendors own it in the new world.

And here’s an important detail: day zero is go-live.

AI value goes down over time because of model drift, data decay, and concept drift. Outcome-based offers include ongoing operations in the promise. You’re not selling a deployment project; you’re selling long-term results.

Trend 2: Sales moves from selling features to consultative design (FDEs go up)

The classic sales engineer is not the most important person in AI delivery. It’s the forward-deployed engineer (FDE), who is a mix of an engineer, a consultant, and a product operator.

Why? Because the last mile needs:

- custom glue code,

- integration that takes security into account,

- redesigning enterprise workflows,

- quick iterations until the result is real.

Slides are not included with FDEs. They bring tools and a sense of ownership.

This changes how sales work:

You are not selling “capabilities.” You’re selling “engineering a result.”

Trend 3: The price for seats goes down, and the AI pricing ladder starts.

Seat pricing worked because people did the work. Now agents do the work.

So the business moves to:

- models of use,

- consumption based on value,

- and finally results.

A useful bridge that many people will use: the price is based on how valuable or difficult the task is, not just how many tokens it costs. It costs more to do complex reasoning and high-value actions than to just get information. The goal is to set prices that match the value of the business while dealing with attribution and volatility.

Trend 4: All lines of service become proactive and automated.

AI doesn’t only change products. It changes everything: support, managed services, customer service, field services, education, and more.

- Support goes from responding to tickets to predicting problems and guiding their resolution.

- Managed services turn into cognitive orchestration, which means not just “monitoring” but also constantly improving AI ROI.

- Customer success changes from LAER to DARE: Design, Activate, Realize, and Evolve.

- Field services become remote diagnosis and “arrive with the right part” accuracy.

- Education turns into AI-driven learning stacks, which include personalized paths, faster content creation, and simulation-first enablement.

The theme stays the same:

Services stop being “heavy on people.” They turn into “AI-assisted, always-on systems.”

Trend 5: The design of organizations changes from silos to value-aligned pods.

AI delivery doesn’t work in siloed organizations because the results affect sales, PS, support, and CS.

Two structures come to light:

Value Engineering Office (VEO)

A central function that sets:

- what results you sell,

- how you measure them,

- and how you make sure that what you promise to sell matches what you actually deliver.

Service delivery pods

Cross-functional teams that work together on a product line or industry outcome, bringing together:

- FDEs,

- data scientists,

- CS,

- and support engineers.

Then you use CoEs (AI/MLOps, data, resource management) to back up the pods for leverage and standardization.

The Five Things That Will Stop Most Businesses

- The transformation paradox: you can’t grow AI services on top of broken operations.

- Data integrity crisis: internal silos and dirty customer data make AI projects stuck in the mud.

- CFO block: it’s hard to change prices because of the addiction to predictability and the variable inference COGS.

- There is a lack of talent because FDEs are “purple squirrels” and AI literacy is not the same across teams.

- No engineering for service offers: you can’t automate “snowflake delivery.” Standardization cannot be changed. The CFO’s resistance isn’t just because they’re conservative; it’s because of the way things are set up. Consumption and outcome models make revenue less stable, and AI makes COGS (GPU-heavy cost curves) less stable as well. One power user can ruin margins if there are no guardrails. If pricing transformation isn’t done with cost visibility, usage controls, and margin governance, it will be shut down.

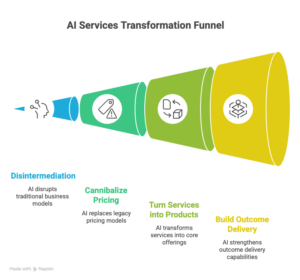

In conclusion, you have to compete or give up.

What it looks like to give in:

- keeping services as an add-on,

- treating AI as features,

- and protecting seat revenue.

That leads to disintermediation.

To compete, you have to “burn the boats”:

Before competitors do,

- cannibalize legacy pricing,

- turn services into products,

- and build outcome delivery muscle as a core skill.

What to do now (real steps)

- Fix the foundation: service engineering, clean delivery data, and standard operating models.

- Set up a VEO by defining value anchors and how you can show them.

- Start moving up the price ladder: pilot value-based consumption → results.

- Check your last mile for data readiness, integration ability, and governance capability.

- Set up an FDE SWAT team: find out what works in the field and then use it on a larger scale.

The time when you could sell software and hope customers would figure it out is over.

The winners will sell results and make sure they are delivered on time.

Leave a Reply